Most North Carolina HOA boards assume reserve studies are legally required. They're not. But here's the hard truth: not being required doesn't mean your board can skip long-term planning. When a $200,000 roof replacement comes due, and your reserve account holds $15,000, that special assessment will land whether you planned for it or not.

North Carolina treats planned communities and condominiums differently under state law. If you serve on an HOA board, you need to understand what Chapter 47F actually requires, what it doesn't, and why your fiduciary duty still demands reserve planning even when the law stays silent. Understanding North Carolina HOA Reserve Study Requirements is critical for every board member, even though the state doesn't mandate them.

This guide walks through North Carolina HOA Reserve Study Requirements, explains the legal framework, and shows you how to protect your community from deferred maintenance and financial instability. Whether your community is a 50-unit townhome development in Charlotte or a 200-unit condo tower in Raleigh, the principles remain the same: infrastructure ages on a predictable schedule, and your board's planning today determines whether homeowners face manageable contributions or financial shocks tomorrow.

Key Takeaways

- North Carolina HOA Reserve Study Requirements do not mandate reserve studies under Chapter 47F, but boards still have a fiduciary duty to plan for major repairs and replacements.

- The North Carolina Condominium Act (Chapter 47C) requires condo developers to include reserve study information in the public offering statement, but ongoing reserve study requirements for established condo associations remain limited.

- Reserve studies combine physical analysis (what will fail and when) with financial analysis (how much to save and how to fund it).

- Special assessments, deferred maintenance, and declining property values are the direct result of inadequate reserve planning.

- Lender requirements from Fannie Mae, FHA, and VA often mandate minimum reserve funding levels, even when state law does not.

- North Carolina boards should update reserve studies every three to five years and adopt funding strategies that match their community's risk tolerance and financial capacity.

- Solume's reserve study tracking tools help North Carolina boards manage capital planning, monitor component lifecycles, and maintain transparency with homeowners.

Legal Framework: North Carolina Planned Community Act and Reserve Study Requirements

The North Carolina Planned Community Act (Chapter 47F) governs homeowners' associations in planned communities. Unlike states such as Florida, California, Nevada, and Washington, North Carolina does not mandate reserve studies for HOAs under Chapter 47F.

Chapter 47F grants boards broad authority to adopt budgets and collect assessments. Section 47F-3-103 allows the executive board to collect assessments for common expenses, including reserves. But the statute does not require boards to fund reserves or commission reserve studies. This creates a permissive framework where boards have the authority to act but not the obligation to do so.

This legislative silence creates a dangerous assumption among many boards. Consider a typical scenario: a 100-unit townhome community in Durham operates for fifteen years without a reserve study. The board keeps assessments low, homeowners are happy, and no one questions the approach. Then the roofs begin failing. The pool deck cracks. The entrance sign topples during a storm. Suddenly, the board faces $400,000 in urgent repairs with $30,000 in reserves. The resulting special assessment of $3,700 per unit creates financial hardship for fixed-income retirees, forces some owners to take out loans, and triggers a wave of delinquencies that further strains the association's finances.

Since reserve study requirements vary significantly by state, North Carolina boards must understand their specific obligations and responsibilities.

Many North Carolina boards interpret "not required" as "optional." That interpretation ignores the fiduciary duty every board member owes to the association and its members. The absence of a statutory mandate does not eliminate the board's responsibility to act prudently, plan for known future expenses, and protect the association's financial health. Courts have consistently held that fiduciary duties exist independent of statutory requirements, and board members who fail to exercise reasonable care in financial planning may face personal liability even in states without explicit reserve study mandates.

Distinction Between HOA (Planned Community) and Condominium Reserve Requirements

North Carolina law treats condominiums and HOAs differently. The North Carolina Condominium Act (Chapter 47C) includes specific provisions related to reserve funding that do not appear in Chapter 47F.

Under Chapter 47C, Section 47C-2-109, a condo developer must include a statement of the status and amount of any reserves for capital expenditures and a statement of any portion of the unit purchase price that will be placed in reserves in the public offering statement. This requirement applies during the developer control period.

Once the developer transfers control to the homeowner-elected board, the ongoing reserve study requirements under Chapter 47C become less prescriptive. The North Carolina General Assembly has not mandated that established condo associations conduct periodic reserve studies, though it does require the association to maintain reserves if the declaration or bylaws call for them.

In practice, both HOAs and condos in North Carolina face the same challenge. The law does not force you to plan, but your community's infrastructure will deteriorate on a predictable schedule whether you plan or not. A condo association in Wilmington and an HOA in Asheville both own roofs that will fail, roads that will crack, and amenities that will require replacement.

The practical distinction matters most during the sales and transition period. Condo buyers receive reserve information upfront, creating an expectation of financial planning and transparency. HOA buyers in planned communities may receive no such information, entering homeownership unaware of the capital planning challenges ahead.

Why 'Not Required' Doesn't Mean 'Not Needed' (Fiduciary Duty Argument)

Every board member in North Carolina owes a fiduciary duty to the association. That duty includes the obligation to act in the best interest of the community, exercise reasonable care, and manage the association's finances responsibly. This duty exists independent of any statutory requirement and applies to every decision the board makes.

Fiduciary duty does not disappear just because the statute stays silent. If your board knows the roof will fail in five years and does nothing to prepare, you are not fulfilling your fiduciary duty. Consider a specific scenario: your board receives a roof inspection report in 2024 stating that the shingles have three to five years of remaining useful life. The board files the report and takes no action. In 2027, the roof begins leaking during a heavy rainstorm. Water damages several units. The board levies a $150,000 special assessment to replace the roof and repair the water damage. Homeowners rightfully ask why the board had three years to prepare but chose to do nothing.

Courts in other states have held boards liable for failing to maintain adequate reserves when that failure results in financial harm to the association. The business judgment rule protects boards that make informed decisions, even if those decisions turn out poorly. But the rule does not protect boards that make no decision at all.

The business judgment rule requires that boards act on an informed basis, in good faith, and in the honest belief that their actions serve the association's best interests. A board that receives a professional assessment identifying future capital needs and chooses to ignore it cannot claim protection under this rule. The board's inaction demonstrates a failure to act on an informed basis.

Many boards assume they are protecting homeowners by keeping assessments low. In reality, they are setting up a special assessment that will hit harder and faster than gradual reserve contributions ever would. A homeowner who pays an extra $50 per month over five years can plan and adjust their budget accordingly. A homeowner who receives a $3,000 special assessment with 30 days' notice faces a financial emergency.

A North Carolina reserve study provides your board with the data needed to make informed decisions. It shows what will fail, when it will fail, and how much you need to save. Without that information, you are guessing. And guessing is not a fiduciary standard.

The documentation provided by a reserve study also protects board members from personal liability. When homeowners question the board's decisions about assessment increases or capital projects, the board can point to the reserve study as the objective, professional basis for its actions.

What Is a Reserve Study and Its Two Core Components (Physical and Financial Analysis)

A reserve study is a budget planning tool that helps boards prepare for major repairs and replacements. It answers two questions: what will break, and how do we pay for it? For boards just starting out, understanding what a reserve study actually measures is the critical first step.

Every reserve study includes two core components: physical analysis and financial analysis. These two components work together to create a complete picture of your community's capital needs and funding strategy.

Physical Analysis

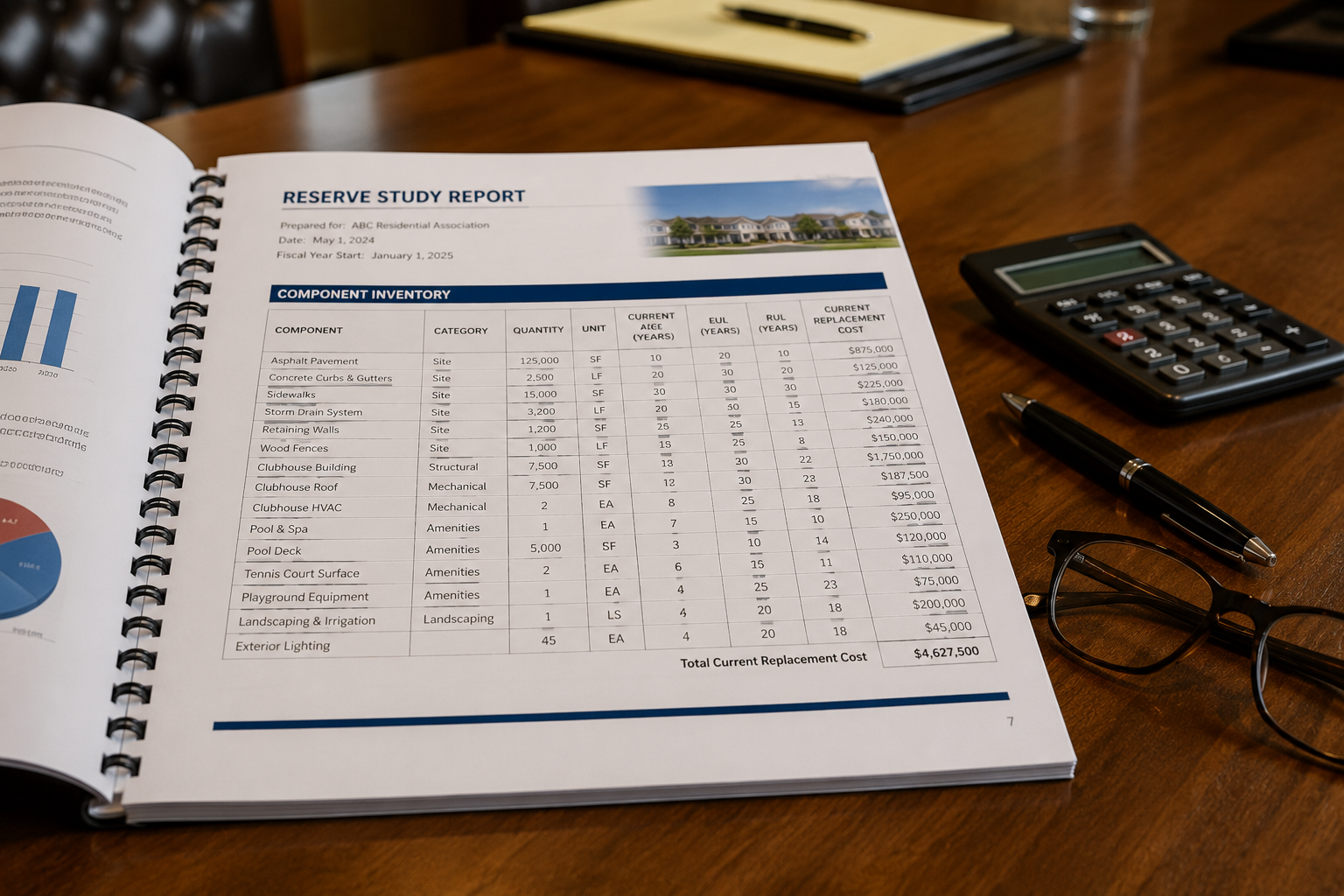

The physical analysis identifies all common-area components with a limited useful life. These are assets the association owns and must replace, such as roofs, roads, pools, HVAC systems, fencing, and pavement.

For each component, the physical analysis estimates the remaining useful life (how many years until replacement), the current replacement cost, and the asset's condition today. Professional organizations like the Appraisal Institute provide standards and methodologies for accurate property assessments.

A qualified reserve specialist conducts a site visit, inspects each component, reviews maintenance records, and develops a replacement schedule. The specialist walks the property, photographs components, measures dimensions, and notes any signs of premature deterioration.

The physical analysis also accounts for regional factors specific to North Carolina. Coastal communities face salt air corrosion and hurricane damage. Mountain communities deal with freeze-thaw cycles that crack pavement and damage masonry. Piedmont communities experience hot, humid summers that accelerate the deterioration of wood components and stress HVAC systems.

Financial Analysis

The financial analysis uses data from the physical analysis to develop a funding plan. It calculates how much the association should contribute to reserves each year to meet future expenses without resorting to special assessments.

The financial analysis evaluates the current reserve balance, projects future income and expenses, and models different funding strategies. It produces a percent-funded metric that indicates how well-funded the reserves are relative to the ideal balance.

The financial analysis also accounts for interest income on reserve balances, inflation adjustments for future costs, and the timing of expenditures. A component that costs $100,000 today will cost more in five years. The analysis applies an inflation factor, typically 2% to 4% annually, to accurately project future replacement costs.

The financial analysis includes cash flow projections that show the reserve balance year by year over a 30-year planning horizon. These projections reveal potential shortfalls before they occur. A board might discover that even with increased contributions, the reserve balance will dip dangerously low in 2029 when three major components need simultaneous replacement.

Together, the physical and financial analyses provide North Carolina boards with a roadmap for reserve funding and long-term planning.

Developer Disclosure Requirements for Condominium Public Offering Statements

Under the North Carolina Condominium Act, Chapter 47C-2-109, a condo developer must provide a public offering statement to prospective buyers before the first conveyance of a unit. The public offering statement must include a statement of the status and amount of any reserves for capital expenditures.

The statute also requires the developer to disclose any portion of the unit purchase price that will be placed in reserves. This gives buyers visibility into how the developer is funding the reserve account during the transition period. The North Carolina Department of Insurance oversees certain aspects of condominium regulation and consumer protection.

Once the developer transfers control to the homeowner-elected board, the ongoing obligation to update or maintain a condominium reserve study is not explicitly required under Chapter 47C. But the initial disclosure sets a baseline. Buyers expect reserves to exist. If the board depletes those reserves or fails to replenish them, property values and marketability suffer.

Many North Carolina condo boards inherit a reserve account from the developer and assume it is adequate. In reality, developer-funded reserves are often insufficient. Developers have an incentive to minimize reserve contributions during the sales period to keep HOA fees low and make units more attractive to buyers.

A condominium reserve study conducted after turnover provides the board with an independent assessment of reserve needs and helps address any shortfalls left by the condo developer. Boards that commission a reserve study within the first year after turnover can identify problems early, communicate transparently with homeowners about the true cost of ownership, and implement gradual contribution increases that are far more palatable than emergency special assessments years later.

Best Practices for North Carolina Boards (Recommended Update Frequency, Funding Strategies)

Even though North Carolina HOA Reserve Study Requirements do not mandate periodic updates, best practices call for updating your reserve study every three to five years. The Community Associations Institute provides extensive guidance on reserve study best practices and board governance.

Components age. Costs change. Inflation, supply chain disruptions, and labor shortages all affect replacement costs. A reserve study from 2018 will not reflect 2026 pricing.

North Carolina boards should also update the reserve study whenever a major component is replaced, the community completes a large capital project, or the board changes its funding strategy. Following the step-by-step process for conducting a reserve study ensures your board captures all necessary information.

Recommended Update Frequency

- Full reserve study with site visit: every five years

- Update with site visit: every three years

- Update without site visit: annually, if the board wants to adjust financial projections without a full physical inspection

Funding Strategies

There are three common funding goal strategies: full funding, threshold funding, and baseline funding.

Full funding means the reserve balance equals the sum of all accumulated depreciation for every component. This is the most conservative approach. It minimizes special assessment risk and maximizes financial stability.

Threshold funding sets a target reserve balance below full funding but above zero. The board sets a percent-funded target (for example, 50% or 70%) and funds to that level. This approach balances affordability with risk.

Baseline funding contributes just enough to cover expenses in the current year or the next few years. It keeps assessments low but increases the likelihood of special assessments when multiple components fail at once.

Most North Carolina boards should aim for threshold funding or full funding. Baseline funding is not a long-term strategy.

Reserve Fund vs Operating Fund: Understanding the Difference

Many volunteer boards confuse the reserve fund and the operating fund. They are not the same, and treating them as interchangeable creates serious financial problems.

The operating fund covers day-to-day expenses: landscaping, utilities, insurance, management fees, routine repairs, and administrative costs. These are predictable, recurring expenses that happen every year.

The reserve fund covers major repairs and replacements: roofs, roads, pools, HVAC systems, and other capital projects with a useful life longer than one year. These expenses are infrequent but large.

If your board uses reserve funds to cover operating shortfalls, you are underfunding future capital needs. If you try to pay for a $150,000 road resurfacing project out of the operating fund, you will either drain your cash reserves or levy a special assessment.

North Carolina boards must maintain a clear separation between the reserve account and the operating fund. Success depends on properly managing reserve funds once your study is complete. Best practices include maintaining separate bank accounts for operating and reserve funds, clearly labeling each account, and prohibiting transfers between accounts except under extraordinary circumstances with full board approval and documentation.

Common Reserve Components for North Carolina Communities (Roofs, Roads, Pools, HVAC)

Every North Carolina HOA and condo association owns common area components that will eventually need replacement. The most common include:

Roofs: Asphalt shingle roofs in North Carolina typically last 20 to 25 years. Metal roofs last longer but cost more. Coastal communities face accelerated wear from salt air and hurricane-force winds.

Roads and pavement: Asphalt roads need resurfacing every 15 to 20 years. Crack sealing and sealcoating extend the useful life. North Carolina's climate, with hot summers and occasional freeze-thaw cycles in winter, creates conditions that accelerate pavement deterioration.

Pools: Pool resurfacing, equipment replacement, and deck repairs are recurring capital expenses. Pool pumps and heaters typically last 10 to 15 years. Pool surfaces need resurfacing every 10 to 20 years, depending on usage and maintenance.

HVAC systems: Clubhouse and common area HVAC systems last 15 to 20 years. Coastal humidity can reduce lifespan. Regular maintenance extends useful life, but even well-maintained systems eventually fail.

Fencing: Wood fencing lasts 10 to 15 years. Vinyl and metal last longer. Wood fencing in North Carolina faces constant challenges from moisture, insects, and rot.

Siding and painting: Exterior siding and paint need replacement or refresh every 10 to 20 years, depending on the material. Wood siding requires more frequent maintenance than vinyl or fiber cement.

Playground equipment: Safety surfacing and equipment replacement follow manufacturer guidelines and safety standards. Playground equipment typically lasts 15 to 20 years, but safety surfacing may need to be replaced every 10 years.

A North Carolina reserve study inventories all of these components, estimates their remaining useful life, and calculates the replacement cost.

Percent Funded Metric and Funding Goal Strategies (Full, Threshold, Baseline)

The percent funded metric is the most important number in your reserve study. It tells you how well-funded your reserves are compared to where they should be.

The formula is simple:

Percent Funded = (Current Reserve Balance) / (Fully Funded Balance) × 100

The fully funded balance is the total accumulated depreciation of all reserve components. If your community owns $1,000,000 in reserve components that have depreciated by $400,000, the fully funded balance is $400,000. If your reserve account holds $200,000, your percent funded is 50%.

A 100% funded percentage means your reserves are fully funded. Every dollar of depreciation is matched by a dollar in the reserve account. A 30% funding level means you are significantly underfunded and face a higher risk of special assessment.

Industry standards suggest:

- 70% to 100% funded: Strong financial position

- 30% to 70% funded: Fair to adequate

- Below 30% funded: Weak position with high special assessment risk

Your funding goal strategy determines your target percent funded. Full funding targets 100%. Threshold funding might target 50% or 70%. Baseline funding accepts a low percentage funded and plans to levy special assessments when needed.

Lender Requirements and Reserve Funding (Fannie Mae, FHA, VA Standards)

Even though North Carolina does not mandate reserve studies, mortgage lenders often do. Fannie Mae, FHA, and VA all have reserve funding requirements that affect whether buyers can obtain financing in your community.

Fannie Mae requires that at least 10% of the association's budget be allocated to reserves. If your community falls below this threshold, buyers may struggle to obtain conventional financing.

FHA requires that the association maintain adequate reserves and prohibits special assessments for deferred maintenance. If your community has a history of large special assessments due to inadequate reserve funding, FHA may refuse to approve loans.

VA has similar requirements and evaluates the association's financial health before approving loans.

If buyers cannot obtain financing in your community, property values decline. Sellers must accept cash offers or offer seller financing, both of which reduce sale prices. A community with inadequate reserves becomes less marketable, and existing homeowners suffer the financial consequences.

Lender requirements create a practical mandate for reserve funding even in states like North Carolina, where the law stays silent. Your board may not be legally required to fund reserves, but if you want to protect property values and maintain marketability, you must meet lender standards.

How Solume Helps North Carolina Boards Track and Manage Reserve Studies

Managing a reserve study is not a one-time task. Component ages and costs change, and boards need to track progress toward funding goals. Solume's reserve study tracking tools help North Carolina boards manage capital planning, monitor component lifecycles, and maintain transparency with homeowners.

Solume allows boards to upload their reserve study, track expenditures against the plan, and update projections as conditions change. The platform provides visual dashboards that show percent funded, upcoming projects, and cash flow projections.

Homeowners can access reserve study information through the Solume platform, increasing transparency and reducing questions about assessment increases. When homeowners understand why assessments are rising and what projects the board is planning, they are more likely to support the board's decisions.

Solume also helps boards schedule reserve study updates, track vendor contracts for capital projects, and document decisions related to reserve funding. This documentation protects board members from liability and demonstrates that the board is fulfilling its fiduciary duty.

Frequently Asked Questions

Are reserve studies required by law in North Carolina?

No. North Carolina does not mandate reserve studies for HOAs under Chapter 47F or for established condo associations under Chapter 47C. However, boards still have a fiduciary duty to plan for major repairs and replacements, and lenders often require adequate reserve funding.

How often should a North Carolina HOA update its reserve study?

Best practices recommend a full reserve study with a site visit every five years, an update with site visit every three years, or an annual financial update without a site visit. Boards should also update the study whenever a major component is replaced or the funding strategy changes.

What happens if our North Carolina HOA doesn't have a reserve study?

Without a reserve study, your board is guessing about future capital needs. This increases the risk of special assessments, deferred maintenance, and declining property values. Lenders may also refuse to approve loans in communities without adequate reserves, making it harder for owners to sell their homes.

Can a North Carolina HOA board use reserve funds for operating expenses?

No. Reserve funds should be kept separate from operating funds and used only for major repairs and replacements. Using reserve funds for operating expenses underfunds future capital needs and violates the board's fiduciary duty.

What is a good percent funded for a North Carolina HOA?

Industry standards suggest 70% to 100% funded is strong, 30% to 70% is fair to adequate, and below 30% is weak with high special assessment risk. Your target percent funded depends on your funding goal strategy and risk tolerance.

Do North Carolina condo associations have different reserve requirements than HOAs?

Yes. Under Chapter 47C, condo developers must disclose reserve information in the public offering statement. However, ongoing reserve study requirements for established condo associations are not mandated. In practice, both condos and HOAs face the same infrastructure challenges and should conduct reserve studies.

Can our North Carolina HOA board conduct its own reserve study?

While boards can attempt a DIY reserve study, professional reserve specialists bring expertise in component lifecycles, replacement costs, and funding strategies that volunteer boards typically lack. A professional study also provides credibility with homeowners and lenders.

What funding strategy should our North Carolina HOA use?

Most boards should aim for threshold funding or full funding. Full funding (100% funded) minimizes the risk of special assessments. Threshold funding (50% to 70% funded) balances affordability with risk. Baseline funding is not a sustainable long-term strategy.

How do we convince homeowners to support increases in reserve funding?

Transparency is key. Share the reserve study with homeowners, explain what components will fail and when, and show the cost difference between gradual reserve contributions and large special assessments. Solume's platform helps boards communicate this information effectively.