A homeowners association in Surfside, Florida, deferred a $9 million repair job on its aging condo tower. In June 2021, the building collapsed, and 98 people died. That tragedy is the most extreme example of what happens when HOA reserve funds fall short. The smaller version plays out constantly: a board discovers the roof needs replacing, there's no money set aside, and every owner gets hit with a $12,000 special assessment they never saw coming. This article explains what reserve funds are, how they differ from your operating budget, how much you should hold, and how to avoid the assessment trap that catches so many boards off guard.

Key Takeaways

- HOA reserve funds are dedicated savings for major, predictable repairs like roofs, pavement, and elevators, kept separate from the operating budget.

- A funded ratio at or above 70% is generally considered strong, while low reserves are the leading cause of surprise special assessments.

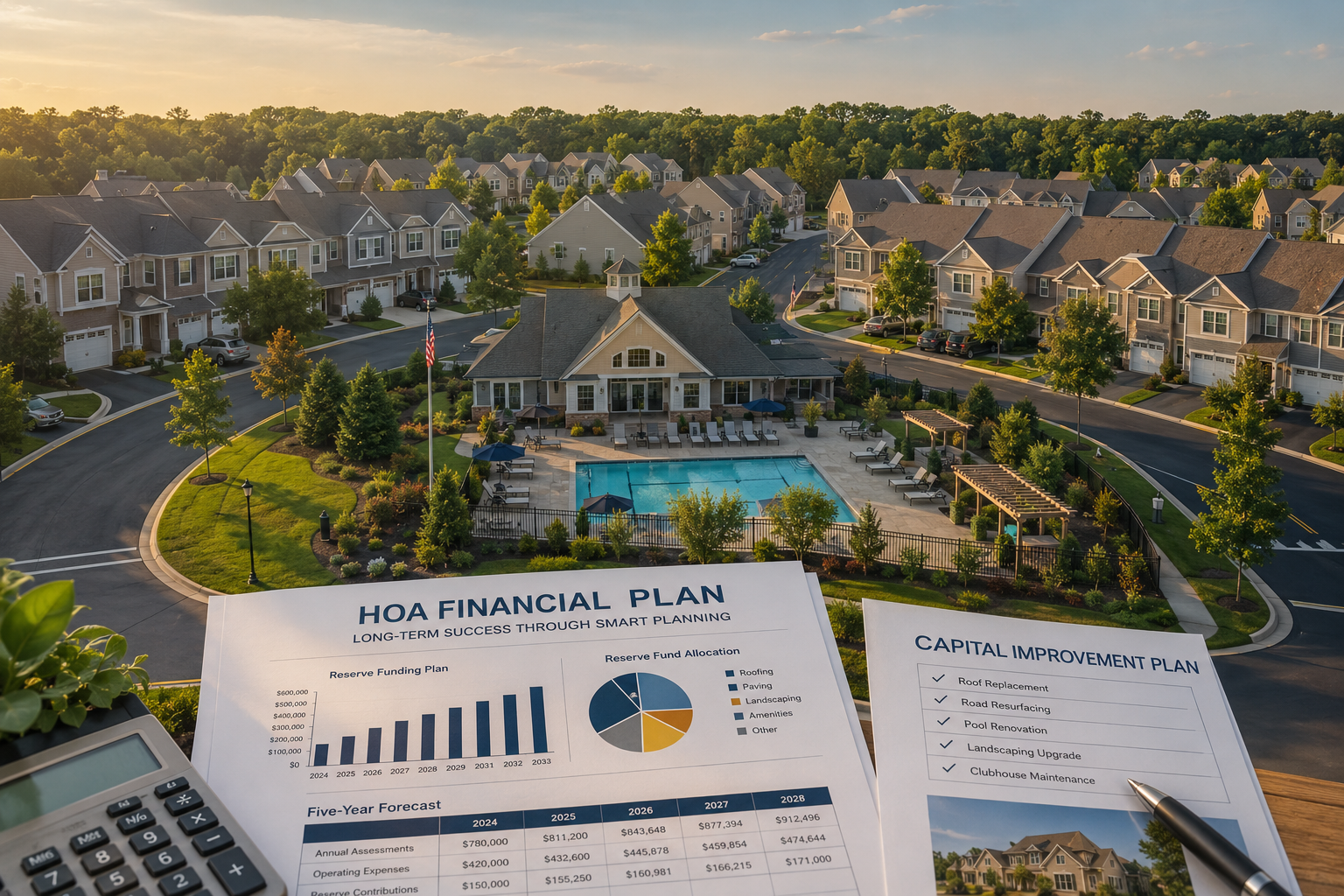

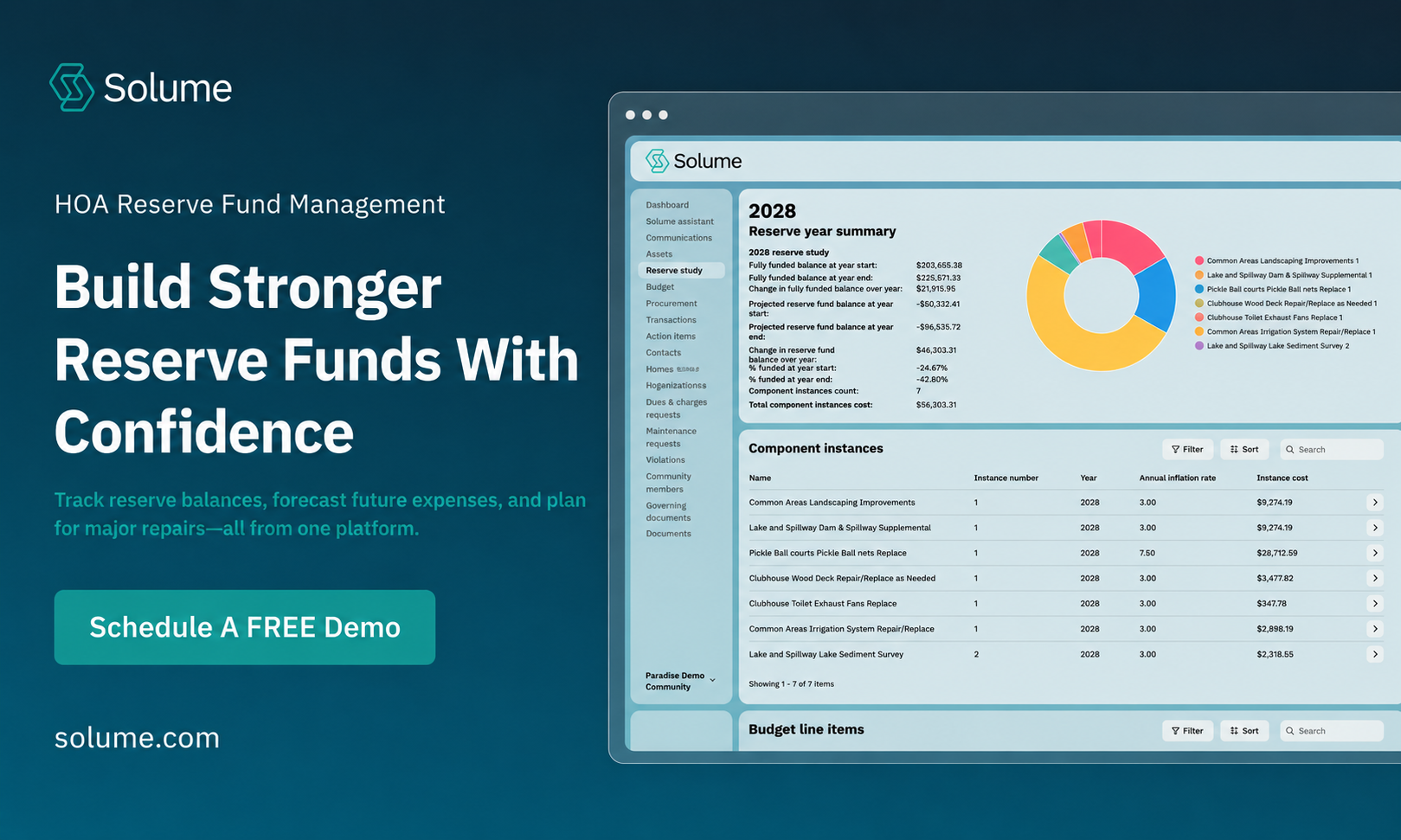

- A reserve study is the foundation of sound reserve planning, mapping component costs and remaining life over a 30-year horizon.

- Underfunded reserves force boards to impose special assessments, take out loans, or defer maintenance, eroding community stability and property values.

- Reserve funds should only be spent on the capital projects they were saved for, with board approval and clear documentation.

What HOA reserve funds are (definition and purpose)

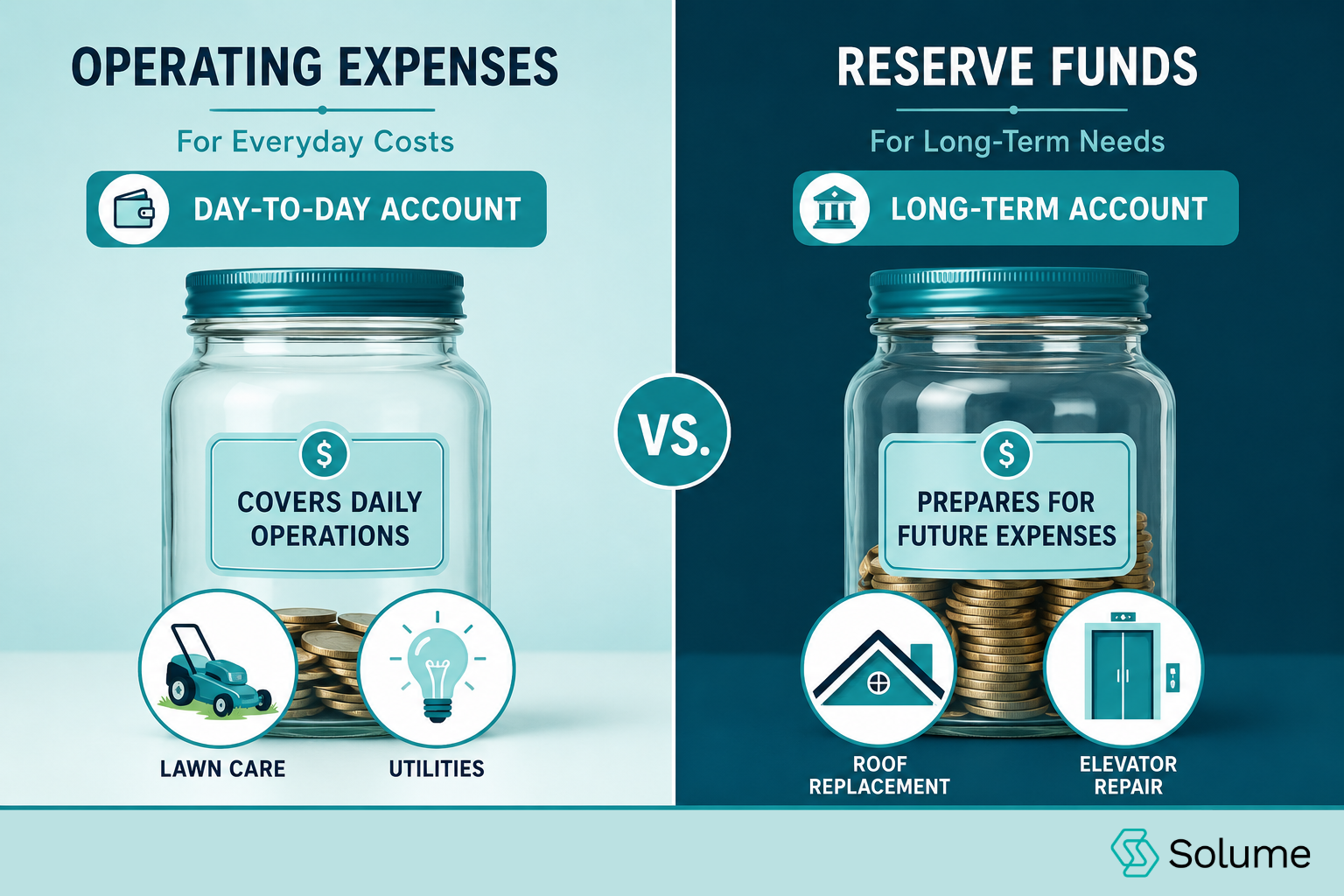

HOA reserve funds are money an association sets aside over time to pay for major repairs and replacements of its common area assets. Think of it as a community savings account earmarked for the big-ticket items every property faces: reroofing the clubhouse, resurfacing the parking lot, replacing an elevator, or repainting every building. These costs are predictable in timing and large in scale. That's why they shouldn't be paid out of the money you use to keep the lights on.

The reason this matters comes down to how these assets age. A roof doesn't fail gradually enough for you to absorb the cost in a single year's budget. It lasts 20 to 30 years, then needs a full replacement that can run into six figures. Reserve funding spreads that cost across the decades. Today's owners pay their fair share instead of dumping it on whoever happens to live there when the bill lands.

Difference between operating funds and reserve funds

The operating fund pays for the day-to-day. Landscaping, utilities, insurance premiums, pool maintenance, management fees, and routine repairs all come out of it. These are recurring, fairly predictable expenses covered by your annual budget and funded through monthly dues. When the operating fund runs a small surplus, most boards roll it into the next year. If you're building that annual budget from scratch, our step-by-step HOA budget guide walks through how to structure operating line items cleanly.

The reserve fund is different. It sits in a separate account, ideally at a separate institution, and it only funds major repairs and replacements identified in your reserve fund study. Mixing the two is one of the most common mistakes self-managed communities make. Here's what actually happens: board members dip into reserves to cover an operating shortfall, tell themselves they will "pay it back," and never do. Now the reserve fund is quietly draining while the funded balance report still looks fine on paper.

Reserve fund accounting keeps these dollars traceable and defensible. Some associations use cash accounting for simplicity. Larger ones tend to use accrual accounting because it more accurately reflects obligations that haven't been paid yet. Small communities without a finance staff can still get this right by following solid bookkeeping practices for small HOAs. The Florida Department of Business and Professional Regulation, which oversees the state's condominium and cooperative associations, enforces separation rules for exactly this reason. Many assume commingling is harmless bookkeeping. In reality, it's how underfunded reserves get hidden until it's too late.

What reserve funds can be used for (major repairs and replacements)

Reserve funds cover the major repairs and replacements of components the association owns and maintains. Roofs, exterior paint, asphalt and concrete, elevators, HVAC systems in shared buildings, pool equipment and resurfacing, fencing, retaining walls, community signage, and clubhouse renovations all qualify. The common thread: these are capital expenses with a limited useful life and a replacement cost too large to absorb in a single year's operating budget.

What reserves are not for: routine maintenance, emergency operating shortfalls, or day-to-day expenses. Patching a small section of pavement is operating. Repaving the entire lot is reserve. Fixing a broken pool pump this month is operating. Replacing the whole pool deck at the end of its 25-year life is reserve. The line isn't always obvious, which is why the reserve study inventories each component and assigns a category.

Every withdrawal should trace back to a component in your reserve study, carry board approval, and appear in the minutes. This protects the board on two fronts. It keeps spending aligned with long-term planning and gives homeowners a record of where their money went. Guarding that community savings account this way is a core board responsibility. It's what separates a trusted board from one facing angry questions at the annual meeting.

Why reserve funds are important (community stability and property values)

Reserve funds are the difference between a community that stays desirable and one that slowly falls apart. When common area assets are maintained on schedule, the property looks good, functions well, and holds its value. When they aren't, the deterioration compounds, and buyers notice.

Property values take a direct hit from weak reserves. Lenders and buyers increasingly ask for reserve fund disclosure before closing. Both Fannie Mae and Freddie Mac now scrutinize condo association reserves before approving mortgages. A community with underfunded reserves can find its units harder to sell and finance. That drag on property values affects every owner, not just the board.

Community stability is the other half of the equation. A healthy reserve level means the board can handle major repairs without emergency special assessments that strain households or fracture neighbor relationships. One 60-unit homeowners association I know went eight years without funding reserves properly, then faced a $480,000 roof and balcony project all at once. The resulting $8,000-per-unit assessment forced three owners into foreclosure. It turned every board meeting into a shouting match for two years. Sound reserve funding prevents that crisis before it starts.

Avoiding special assessments through proper funding

Special assessments occur when reserve planning fails. The board discovers a major expense, finds the reserve fund can't cover it, and has no choice but to bill owners directly. That's often thousands of dollars each, on short notice. Most boards assume they'll never need one. Then a component reaches the end of its life ahead of schedule, and suddenly they do.

The fix is boring and effective: fund reserves steadily so the balance is there when the project arrives. A properly funded reserve turns a $200,000 roof from an emergency into a planned expense budgeted years in advance. Instead of a shock to owners, the cost gets collected gradually through modest reserve contributions built into monthly dues, sparing them from unexpected costs.

Partial funding still leaves you exposed. Some boards adopt a threshold or baseline strategy that keeps the balance above zero but well below the ideal. That's better than nothing, but a large enough or early enough failure can still trigger an assessment. The safer path is to align your reserve contribution with what the reserve fund study recommends and revisit it every year during the budget cycle. Special assessments are often a symptom of underfunded reserves, not bad luck.

How much an HOA should keep in reserves (funding levels and rules of thumb)

The honest answer is that a reserve study tells you, and no generic figure replaces one. That said, boards want a starting point, so here are the common reserve rule-of-thumb benchmarks. Many advisors suggest reserves equal to 25% to 40% of your annual budget. A more precise measure is the funded ratio, which compares your current balance to the fully funded balance your reserve study calculates.

Here's how to read the funded ratio. Fully funded reserves sit at or near 100% of the calculated ideal. A reserve level at or above 70% is generally considered strong. Between 30% and 70% is a caution zone. A rate below 30% signals a high risk of special assessments. This reserve rule of thumb gives boards a quick pulse check between formal studies.

Requirements vary significantly by state. California HOA reserve fund laws require associations to conduct a reserve study at least every three years and disclose funding status annually to members, a mandate spelled out in California Civil Code Section 5550 reserve study requirement. Florida mandates structural integrity reserve studies for many condo associations, with the details laid out in Florida Statute 718.112 on condo reserves; our breakdown of Florida's reserve funding rules explains what that means in practice. Nevada, Colorado, and others have their own rules. Because the specifics differ, check the full picture of reserve study requirements by state and confirm your compliance obligations against your state's HOA or condominium statute, then consult your association attorney for guidance specific to your community. Don't rely on a national rule of thumb where state law governs.

Risks and consequences of underfunded reserves

Underfunded reserves don't announce themselves. Everything looks fine until a major component fails, and then the consequences arrive all at once. The most immediate is the special assessment: a lump-sum bill that can run from a few hundred to tens of thousands of dollars per owner. For households on fixed incomes, that's not an inconvenience. It's a genuine financial crisis.

When owners can't or won't pay, boards turn to bank loans secured against future assessments. These carry interest, add ongoing debt, and often require the very funding increases board members avoided in the first place. The root cause is almost always the same: years of setting monthly dues too low to build reserves, because raising dues is unpopular and volunteer boards want to keep the peace.

Then there's deferred maintenance, the slowest and most damaging outcome. Without money, the board postpones repairs. Postponed repairs get worse and more expensive. A small roof leak can lead to structural damage. Cracked pavement becomes a full teardown. A missing financial cushion means these unexpected costs quietly destroy community stability and drag down property values. The longer it runs, the harder the recovery. The Surfside collapse was deferred maintenance taken to its catastrophic conclusion.

Using software to automate reserve planning and transparency

For self-managed communities, the hardest part of reserve funding isn't understanding it. It's keeping up with the accounting, the disclosures, and the annual updates without a dedicated finance staff. Spreadsheets get outdated. Reserve studies sit in a drawer. And when a homeowner asks where the money is, the board scrambles.

This is where purpose-built tools help. Solume provides boards with automated reserve study tools and compliance tracking, so your funding plan stays current and your state's disclosure and compliance requirements don't slip through the cracks. Its financial management tools built for boards handle budgeting, tracking, and reserve fund accounting in one place, keeping your operating fund and reserve fund cleanly separated instead of tangled in a shared ledger.

Transparency is the other payoff. When reserve balances, contributions, and spending are visible to owners in real time, the trust gap between board and community closes. Homeowners stop assuming the worst because they can see exactly where their dues go. That kind of open reserve fund accounting is difficult to maintain by hand and straightforward with the right platform. It frees volunteer board members to focus on decisions instead of data entry.

If your board wants a clearer way to manage reserve planning, financial transparency, and compliance without leaning on a management company, you can book a 15-minute call to see if Solume fits your community. It's a short conversation, not a sales pitch, and you'll walk away knowing whether it's the right tool for how your board actually works.

Frequently Asked Questions

How much should an HOA keep in reserve funds?

Financial experts often recommend reserves equal to 25% to 40% of the annual operating budget, though a more precise benchmark is 70% to 100% of the fully funded balance identified in a reserve study. The right target depends on your community's size, its common elements, and state-specific requirements.

What does a 70% funded reserve mean?

A 70% funded reserve means the HOA currently holds 70% of the money it would ideally have saved to cover all projected replacement costs at that point in time. Anything at or above 70% is generally considered strong, while below 30% signals a high risk of special assessments.

Can a board withdraw money from the reserve fund?

Yes, but reserve funds should only be used for the major capital projects identified in the reserve study, not to plug operating shortfalls. Many states require board approval, documentation, and sometimes a repayment plan when funds are borrowed for non-reserve purposes.

What happens if our HOA's reserves are underfunded?

Underfunded reserves often lead to special assessments or emergency loans when a major repair comes due, which can strain homeowners financially. They also cause deferred maintenance that accelerates deterioration, raises future costs, and can lower property values across the community.

Do we really need a reserve fund if nothing major is broken right now?

Here's the hard truth: reserve funds exist precisely because big expenses are predictable but distant, so the money must accumulate before the roof or pavement fails. Skipping reserves doesn't avoid the cost; it just shifts it to a surprise special assessment later.

How are reserve fund contributions actually calculated?

A reserve study inventories every major common-area component, estimates its remaining useful life and replacement cost, then sets a funding plan using a method like full funding, baseline funding, or threshold funding. Contributions are collected through regular homeowner assessments so the balance builds ahead of each project.