Many Massachusetts condominium boards assume that setting aside some money in a reserve account is enough to meet their legal obligations. However, while Massachusetts law requires associations to maintain an adequate replacement reserve fund, it does not define what "adequate" means or require a formal reserve study. This leaves many boards navigating long-term capital planning without a clear roadmap.

The challenge is that major expenses such as roof replacements, pavement resurfacing, siding repairs, and mechanical system upgrades are inevitable. Without proper planning, these costs can lead to significant special assessments, financial strain for homeowners, and even difficulties with mortgage approvals. Massachusetts communities also face unique maintenance pressures from harsh New England winters, freeze-thaw cycles, coastal weather exposure, and seasonal storms that can accelerate deterioration.

Key Takeaways

- Massachusetts HOA Reserve Study Requirements in Massachusetts include maintaining an adequate replacement reserve fund under Chapter 183A Section 10(i), but the state does not mandate reserve studies

- Most boards assume they're compliant if they're setting aside some money. In reality, "adequate" means enough to cover projected replacement costs, not just an arbitrary percentage

- Reserve studies provide the financial roadmap boards need to determine what "adequate" actually means for their community

- Lender requirements from Fannie Mae and Freddie Mac often trigger the need for reserve studies, even when state law doesn't

- Massachusetts boards face unique reserve pressures from New England climate conditions, including freeze-thaw cycles and nor'easters that accelerate building deterioration

- Self-managed communities can use software tools to conduct preliminary reserve assessments and track long-term capital needs

Massachusetts Chapter 183A Section 10(i) Requirement for Adequate Replacement Reserve Fund

Massachusetts General Laws Chapter 183A Section 10(m) establishes a clear legal obligation: condominium associations must maintain an adequate replacement reserve fund for capital improvements and major repairs.

Here's what the statute actually says. The organization of unit owners must maintain a replacement reserve fund "unless the master deed or bylaws of the organization provide otherwise, or unless at least two-thirds of the votes of all unit owners entitled to vote at a meeting duly called for such purpose vote not to maintain such fund."

That waiver provision creates a dangerous trap. Many Massachusetts condo associations assume they can vote to eliminate reserves and avoid the problem entirely. But that decision exposes the HOA board to personal liability if the community faces a major repair without adequate funds.

The law doesn't specify how much money constitutes "adequate." It doesn't require a reserve study. It simply requires that whatever you set aside be sufficient to meet your actual obligations.

Most Massachusetts boards discover what "adequate" means only when they need to replace a roof or repave parking lots and realize they're $200,000 short.

Distinction Between Reserve Studies (Not Required) vs. Reserve Fund Maintenance (Required by Law)

Massachusetts HOA Reserve Study Requirements in Massachusetts don't mandate formal studies. But the law does require reserve fund maintenance. That distinction confuses most volunteer boards.

A reserve fund is the bank account where you accumulate money for future replacements. Reserve fund maintenance means you're actually putting money into that account and not raiding it for operating expenses.

A reserve study is the engineering and financial analysis that tells you how much money you should be accumulating. It inventories your common property, estimates when each component will need replacement, calculates replacement costs, and projects a 30-year funding plan.

The law requires the fund. The study tells you whether your fund is adequate. For boards looking to understand reserve study requirements across all 50 states, Massachusetts represents a middle ground: reserves are required, but formal studies are not mandated.

Think of it this way: Massachusetts law requires you to save for retirement, but doesn't require you to calculate how much you'll actually need. Most people who skip that calculation end up broke at 65.

The same principle applies to HOA board members. You can maintain a reserve fund that's completely inadequate and still be technically compliant with Chapter 183A. But when the assessment comes due, your homeowners will pay the price.

Recommended Reserve Funding Levels and Adequacy Benchmarks in Massachusetts

So what does "adequate" actually mean in practice?

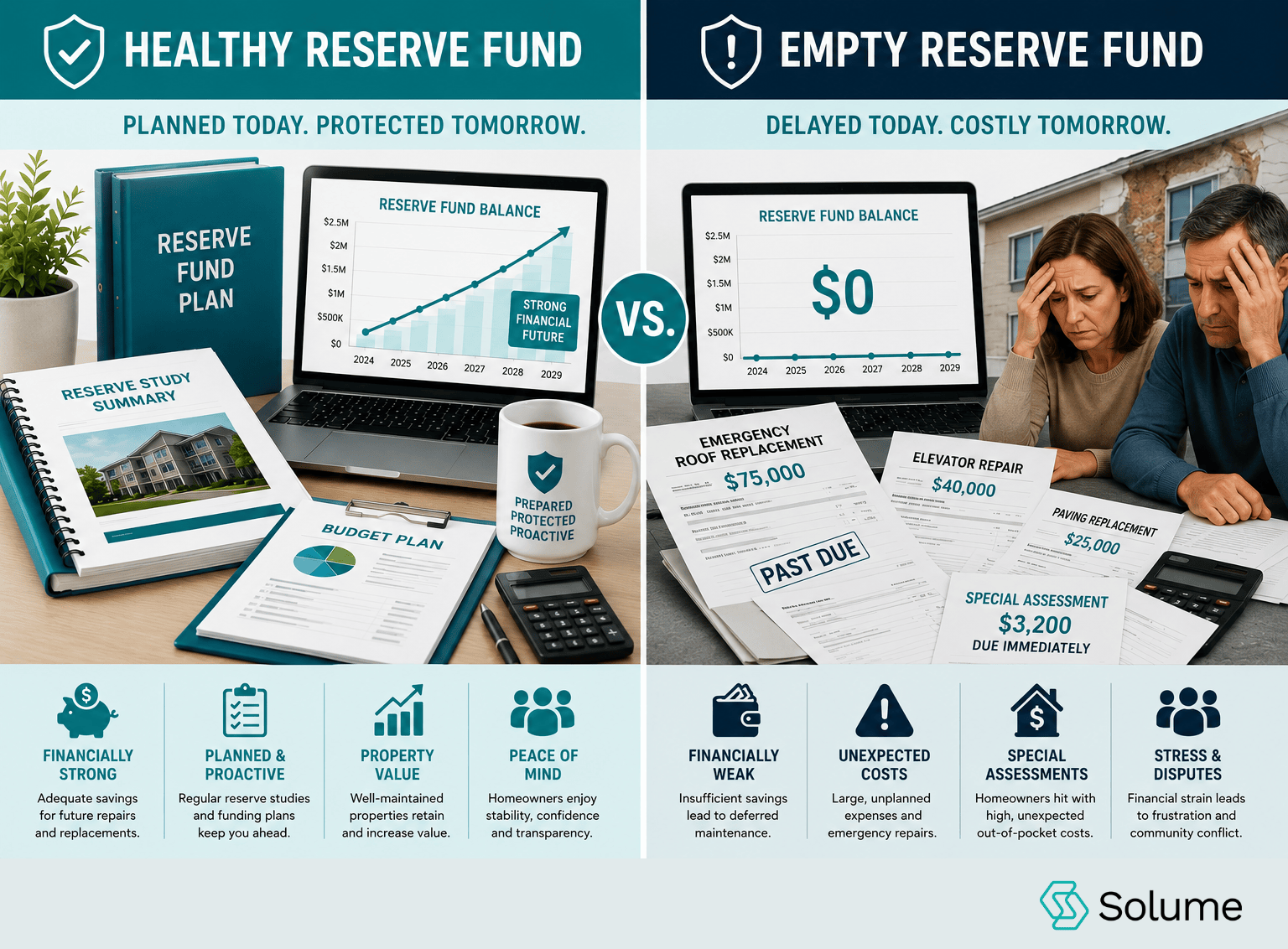

Industry standards suggest reserve funds should be funded at 70% or higher of the ideal balance. That means if your reserve planning projects you should have $500,000 in reserves today to cover your 30-year funding plan, you should have at least $350,000 in the bank.

Funding below 30% is considered critically underfunded. Boards operating at that level are one major failure away from a special assessment.

Many Massachusetts condo associations follow an informal 10% reserve rule, setting aside 10% of their annual budget for reserves. That approach is better than nothing, but it's arbitrary. A community with aging infrastructure needs far more than 10%. A newer development might need less.

Fannie Mae and Freddie Mac impose their own benchmarks. Both lenders require at least 10% of the operating budget to be allocated to reserves for buildings three stories or higher. They also require that the reserve balance equal at least 10% of the current replacement cost of all major components.

If your community has $3 million in insurable replacement value for roofs, siding, pavement, and mechanical systems, Fannie Mae expects you to maintain at least $300,000 in reserves.

Lender requirements often force the issue. A unit owner trying to sell discovers their buyer can't get financing because the association's reserves don't meet Fannie Mae standards. Suddenly, the board is scrambling to commission a reserve study and raise contributions.

Step-by-Step Compliance Roadmap for Massachusetts Boards

Massachusetts boards can achieve compliance and reduce long-term financial risk by following this roadmap:

Step 1: Review your governing documents. Check whether your master deed or bylaws include a waiver provision under Section 10(i). If your community voted to waive reserves, understand that the decision exposes the board to fiduciary duty claims if a major repair creates financial hardship.

Step 2: Inventory your common property. List every component the condominium association is responsible for maintaining: roofs, siding, pavement, pools, clubhouses, elevators, HVAC systems, and site improvements. If you don't know what you own, you can't plan to replace it.

Step 3: Estimate component lifespan and replacement cost. Determine how many years of useful life remain for each major component. Get contractor quotes or use industry benchmarks to estimate the cost of the replacement in future dollars.

Step 4: Calculate your current funding level. Divide your current reserve balance by the total projected replacement cost of all components. If you have $200,000 in reserves and $1 million in projected costs over the next 10 years, you're 20% funded.

Step 5: Develop a reserve contribution plan. Determine how much the association needs to contribute each month or year to achieve adequate funding. Most boards phase in increases over three to five years to avoid sticker shock. Proper planning includes strategies to avoid special assessments that can burden homeowners.

Step 6: Communicate the plan to homeowners. Transparency matters. Explain why reserve contributions are increasing, what components the funds will cover, and how the plan protects property values. Most homeowners accept higher fees when they understand the alternative is a special assessment.

Step 7: Update the plan every three to five years. Reserve planning isn't static. Costs change. Components fail earlier or last longer than expected. Boards should refresh their analysis regularly.

Boards that skip this process often discover the problem only when a lender rejects a buyer's mortgage application or a major component fails without warning.

When Massachusetts Associations Typically Need a Reserve Study (Aging Buildings, Post-Storm, Refinancing)

Even though Massachusetts reserve study requirements don't mandate formal studies, certain situations make them necessary.

Aging buildings. Communities built in the 1970s and 1980s are hitting the point where multiple major components fail simultaneously. Roofs, siding, pavement, and mechanical systems all reach the end of their lifespan at roughly the same time. Boards managing older properties need reserve planning to avoid catastrophic special assessments.

Post-storm damage. Nor'easters and severe winter weather accelerate deterioration in Massachusetts. After a major storm, boards should reassess the lifespan of components. The New England climate, with freeze-thaw cycles, can reduce the expected service life of pavement and masonry by years.

Refinancing or sale transactions. Fannie Mae and Freddie Mac often require a reserve study as a condition of loan approval. If unit owners in your community are struggling to sell because buyers can't get financing, the association needs a reserve study.

Transition from developer control. When a new community transitions from the developer to the homeowners, the volunteer board inherits responsibility for components they didn't choose and may not understand. A reserve study provides the baseline financial plan the new board needs.

Lender or insurance company request. Some insurance carriers require reserve studies before renewing coverage for older buildings. Lenders refinancing association loans may require updated reserve analysis.

Deferred maintenance accumulation. If your community has been deferring maintenance for years, a reserve study quantifies the problem. It gives the board a defensible plan to present to homeowners when explaining why fees must increase.

The reserve study cost typically ranges from $2,500 to $7,000, depending on the community's size and complexity. A Level 1 reserve study includes a full site inspection and detailed component inventory. A Level 2 study uses association-provided data without a site visit. A Level 3 reserve study update refreshes an existing study without re-inventorying components.

Most Massachusetts boards should start with a Level 1 reserve study to establish an accurate baseline.

Massachusetts-Specific Case Studies of Reserve Failures and Deferred Maintenance Consequences

Reserve failures aren't theoretical. Massachusetts communities have faced serious consequences when boards deferred maintenance or underfunded reserves.

One Boston-area condominium association deferred roof replacement for three years to avoid raising fees. When the roof finally failed during a winter storm, water damage affected 18 units. The association faced a $450,000 special assessment, plus individual unit-owner claims for interior damage. The board's decision to delay a planned $180,000 roof replacement ultimately cost the community more than twice that amount.

A Worcester condominium discovered its parking lot had deteriorated beyond repair. The board had been patching potholes for a decade rather than planning for full resurfacing. When the city issued a code violation notice, the association had $12,000 in reserves and a $95,000 repair bill. The resulting special assessment caused three unit owners to default on their mortgages.

A Cape Cod community waived reserve contributions under Section 10(i) for eight consecutive years. When the seawall failed after a nor'easter, the association had no funds to make emergency repairs. The board took out a loan at 9% interest, saddling homeowners with both loan payments and increased insurance premiums after the carrier threatened to drop coverage.

These situations share a common pattern. Boards prioritized short-term fee stability over long-term financial responsibility. Homeowners paid far more in the end than they would have through gradual reserve contributions. Proper management of HOA reserve funds could have prevented these crises.

The hard truth is that deferred maintenance doesn't save money. It just transfers the cost to whoever happens to own the unit when the bill comes due.

How Self-Managed Massachusetts Boards Can Conduct DIY Reserve Assessments Using Software Tools

A self-managed HOA doesn't need to hire a reserve study professional to begin planning. Several practical tools allow volunteer boards to conduct preliminary reserve assessments.

Start with a spreadsheet. List every major component the association maintains. Record the installation date, expected lifespan, and estimated replacement cost. Calculate the annual reserve contribution needed by dividing replacement cost by remaining years of useful life.

For example, if your roof was installed in 2010, has a 25-year lifespan, and will cost $150,000 to replace, you have roughly 9 years remaining. Divide $150,000 by 9 years to get an annual reserve contribution of $16,667 for the roof alone. Repeat for every component.

Reserve study software can automate this process. Tools like Reserve Advisor and Reserve Study Pro allow boards to input component data and generate funding projections. These platforms cost between $300 and $1,200 annually, far less than commissioning a professional study. Many boards also benefit from HOA management software designed for self-managed communities that includes reserve tracking features.

Solume's reserve study integration allows a self-managed HOA in Massachusetts to track component lifespan, project replacement costs, and monitor reserve funding levels within the same platform they use for accounting and vendor management. The system flags components approaching end of life and calculates the reserve contribution needed to maintain adequate funding.

DIY assessments have limitations. Volunteer boards often underestimate replacement costs or misjudge component lifespan. But even a rough reserve assessment is better than no planning at all.

Boards should treat DIY reserve assessments as a starting point. Use the preliminary analysis to identify major funding gaps, then commission a professional Level 1 reserve study to validate assumptions and refine the plan.

The goal isn't perfection. The goal is to stop operating blind.

Massachusetts HOA Reserve Study Requirements in Massachusetts demand that boards maintain adequate reserves under Chapter 183A, even though formal studies aren't mandated. The boards that succeed are the ones that treat "adequate" as a specific financial target, not a vague aspiration. They inventory their components, calculate replacement costs, and fund reserves based on actual projections rather than arbitrary percentages.

If your Massachusetts board needs help tracking reserve funding, managing capital improvements, and meeting your fiduciary duty under Chapter 183A, explore your options with Solume's reserve planning tools designed specifically for self-managed communities. The platform integrates reserve tracking with accounting and vendor management so you can stop guessing and start planning with confidence.

Frequently Asked Questions

What does Massachusetts law require for condo reserve funds?

Chapter 183A Section 10(i) requires Massachusetts condo associations to maintain an adequate replacement reserve fund unless the master deed waives it or two-thirds of unit owners vote to eliminate it. The law doesn't specify an amount or require a reserve study, but boards must ensure the fund is sufficient to cover projected capital improvements.

How often should Massachusetts HOAs update their reserve studies?

Most reserve professionals recommend a reserve study update every three to five years. Boards should also update after major unexpected repairs, significant cost increases, or changes in component lifespans due to climate factors such as freeze-thaw cycles.

What components should be included in a reserve study?

Reserve planning should cover all major common property components with limited lifespans and high replacement costs: roofs, siding, pavement, pools, clubhouses, elevators, HVAC systems, site drainage, and structural elements. Operating budget items like landscaping and routine maintenance are excluded.

Is a reserve study worth it if Massachusetts doesn't require one?

Yes, because "adequate" under Chapter 183A means sufficient to cover actual costs. Without a reserve study, boards are guessing, and a $5,000 reserve study cost can prevent a $200,000 special assessment by identifying funding gaps before components fail.

What happens if a Massachusetts HOA doesn't maintain adequate reserves?

Boards that fail to maintain adequate reserves expose themselves to fiduciary duty claims under the business judgment rule. Unit owners can sue if inadequate reserves lead to special assessments that could have been avoided through proper planning.