A South Carolina HOA board discovers its pool heater has failed in July, peak swim season. The replacement cost is $18,000. The reserve account has $3,200. The board's only options are a special assessment that will anger homeowners or an emergency loan that will drain next year's budget.

Here's the hard truth: South Carolina doesn't require HOAs to conduct reserve studies. But that doesn't mean your board can skip them. Without understanding HOA Reserve Study Requirements in South Carolina, you're flying blind on the most expensive decisions your community will face. You don't know what's about to fail, how much it will cost to replace, or whether you have enough money saved to cover it.

This guide walks through everything South Carolina boards need to know about reserve studies: what the law actually says, why reserve planning still matters, how to conduct a study, and how to use the data for long-term financial stability.

Key Takeaways

- South Carolina has no statewide law requiring HOAs to conduct reserve studies under the HOA Reserve Study Requirements, but your governing documents may still require them.

- Reserve studies protect boards from special assessments, deferred maintenance, and potential liability for failing to plan.

- A complete reserve study includes a physical analysis of all common elements and a financial analysis showing how much to save each year.

- Most South Carolina communities should update their reserve study every three to five years, with annual updates to the funding plan.

- A self-managed HOA can track and update reserve studies using spreadsheets or software designed for volunteer boards.

- Reserve study data gives your board the transparency and credibility needed to justify fee increases and avoid financial surprises.

South Carolina Legal Framework for HOAs and Reserve Planning

South Carolina has two main statutes governing community associations: the South Carolina Homeowners Association Act (for planned communities) and the South Carolina Horizontal Property Act (for condominiums). Neither law explicitly requires boards to conduct reserve studies or maintain HOA reserve funds.

That makes South Carolina different from states like Florida, Nevada, or Washington, where reserve study requirements vary significantly by state. But the absence of a state mandate doesn't eliminate your board's responsibility to plan for capital expenses.

Your governing documents (the declaration, bylaws, and articles of incorporation) may still require reserve planning. Many older communities in South Carolina were established with documents that reference reserve accounts or capital improvement funds. If your documents mention reserves, your board is legally obligated to follow those provisions.

Even if your documents don't mention reserves, your board still has a fiduciary duty to manage the association's finances responsibly. That duty includes planning for predictable expenses like roof replacements, asphalt resurfacing, and pool equipment. Courts have held boards liable for failing to maintain common property, and deferred maintenance often stems from inadequate reserve funding.

What South Carolina Law Actually Says About Reserve Funds

The South Carolina Homeowners Association Act (SC Code § 27-30-110 et seq.) gives HOAs broad authority to collect assessments and manage association funds. The law allows boards to establish reserve accounts, but it doesn't require them.

The South Carolina Code of Laws Title 27, Chapter 31, which governs condominiums, is similarly silent on reserve study requirements. The act requires a condo association to maintain common elements and collect adequate assessments, but it doesn't specify how boards should calculate those assessments or plan for future replacements.

Federal lending requirements often fill the gap where state law is silent. FHA requirements and Fannie Mae guidelines both require reserve studies for condo associations seeking mortgage approval for buyers. If your community wants to remain eligible for FHA or Fannie Mae financing, you need a reserve study, regardless of what state law says. This is the mechanism that makes reserve studies practically mandatory for many South Carolina condominiums, even in the absence of a state law.

For planned communities (traditional HOAs), the lending requirements are less strict. But lenders still review reserve balances when underwriting loans in HOA communities. Low or nonexistent reserves can make it harder for buyers to secure financing, which directly affects property values.

Why Reserve Studies Still Matter Without a State Mandate

Just because South Carolina doesn't require reserve studies doesn't mean your board should skip them. Reserve studies are one of the most practical tools a board can use to avoid financial chaos.

Special assessments are the most visible consequence of poor reserve planning. When a major expense comes due, and the association doesn't have the money saved, the board has two options: borrow money or pass a special assessment. Both options are unpopular with homeowners, and both could have been avoided with proper reserve funding.

Deferred maintenance is the hidden cost. Boards that don't plan for capital expenses often delay repairs to avoid raising fees. That delay makes the problem worse. A roof that could have been patched five years ago now needs full replacement. A pool deck that needed resurfacing now has structural damage. Deferred maintenance always costs more in the long run because deterioration accelerates once components pass their optimal maintenance window.

Transparency builds trust. Homeowners want to know where their money is going. A reserve study gives your board a clear, defensible plan for future expenses. When you propose a fee increase, you can cite the reserve study and explain exactly why it is necessary. Without that data, homeowners assume the board is mismanaging funds.

Property values depend on financial stability. Buyers and lenders look at reserve balances when evaluating a community. A well-funded reserve account signals that the association is financially stable. An empty reserve account raises red flags. Communities with strong reserves sell faster and for higher prices than communities with deferred maintenance and special assessments.

Board liability is real. Board members are volunteers, but that doesn't shield them from liability. If your board fails to maintain common property and a homeowner is injured, the board could be held personally liable. If your board allows the community to deteriorate and property values drop, homeowners can sue for breach of fiduciary duty. A reserve study shows that your board took reasonable steps to plan for the future.

What Is a Reserve Study: Components and Analysis

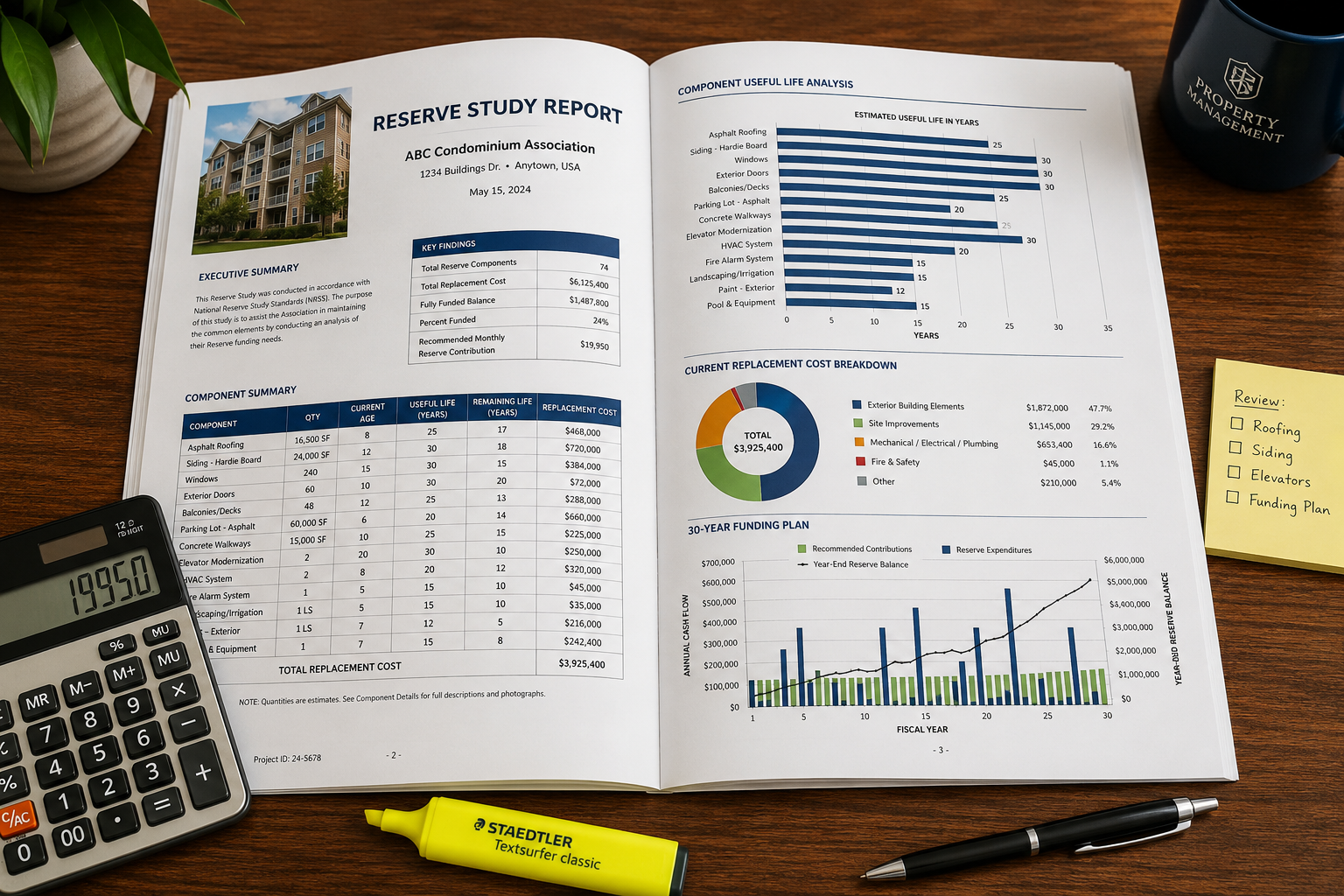

A reserve study is a budget forecast for everything your association owns that will eventually need to be replaced. It tells you what you have, how long it will last, how much it will cost to replace, and how much you need to save each year to pay for it.

Every complete reserve study has two parts: a physical analysis and a financial analysis. Understanding what a reserve study actually includes helps boards make informed decisions about their community's financial future.

The physical analysis creates an asset inventory of all common elements. A reserve study professional walks your property and documents every major component: roofs, siding, pavement, pools, clubhouses, fences, gates, playgrounds, and more. For each component, the professional estimates the remaining useful life and the replacement cost.

Useful life is the period during which the component will last before it needs to be replaced. A typical asphalt parking lot might have a useful life of 20 to 25 years. A pool heater might last 10 to 15 years. The physical analysis documents the current condition of each component and estimates when it will need attention.

Replacement cost is what it will cost to replace the component when the time comes. The reserve study professional uses current pricing and adjusts for inflation. This gives your board a realistic target for how much money needs to be in the reserve fund when the expense comes due.

The financial analysis shows how much to save each year. Once the physical analysis is complete, the reserve study professional calculates how much your association should contribute to reserves annually. This calculation depends on your current reserve balance, your upcoming expenses, and your funding strategy.

The financial analysis also calculates percent funded, which is the ratio of your current reserve balance to the amount you should have saved by now. A 100% funded percentage means your reserves are fully funded. A 30% funding level means you're significantly underfunded and at high risk of special assessments.

The output of a reserve study is a funding plan showing how much your board should contribute to reserves each year over the next 30 years. This plan accounts for inflation, interest, and the timing of major expenses.

Recommended Reserve Study Frequency and Update Cycles

A full reserve study should be conducted every three to five years. This gives your board a fresh physical analysis and updated replacement costs. Construction costs change, component conditions change, and your community's needs evolve. A reserve study from 2015 is no longer accurate in 2025.

Between full studies, your board should update the financial analysis annually. This is called a reserve study update. An update adjusts the funding plan based on actual expenses, interest earned, and changes in your reserve balance. Most reserve study professionals offer annual updates at a fraction of the cost of a full study.

For South Carolina communities, the recommended cycle looks like this:

- Year 1: Full reserve study with physical analysis and financial analysis.

- Year 2: Update the financial analysis only.

- Year 3: Update the financial analysis only.

- Year 4: Full reserve study with new physical analysis.

- Year 5: Update the financial analysis only.

This cycle keeps your reserve plan accurate without requiring a full site inspection every year.

Some boards try to stretch a reserve study for 10 or 15 years. That's a mistake. Component conditions change, replacement costs increase, and your funding plan becomes outdated. By the time you realize the plan is wrong, you're already behind.

A self-managed HOA often asks whether it can skip the professional study and do it itself. The short answer is yes, but it's risky. Reserve studies require knowledge of construction costs, useful life estimates, and financial modeling. If you underestimate costs or overestimate useful life, your funding plan will fail. Most boards find that paying for a professional study is worth the peace of mind.

Step-by-Step Guide to Conducting a Reserve Study in South Carolina

If your board is ready to conduct a reserve study, here's how the process works. Conducting a reserve study for your community requires careful planning and professional expertise.

Step 1: Review your governing documents. Check whether your declaration or bylaws require reserve studies or reserve funding. If they do, follow those requirements. If they don't, your board still has the authority to establish a reserve account and commission a study.

Step 2: Hire a reserve study professional. Look for a credentialed reserve specialist with experience in South Carolina communities. The two main credentials are Reserve Specialist (RS) from the Community Associations Institute and Professional Reserve Analyst (PRA) from the Association of Professional Reserve Analysts. Ask for references from other South Carolina associations and review sample reports before hiring.

Step 3: Provide access to the property and financial records. The reserve study professional will need to walk your property and inspect all common elements. They'll also need your current reserve balance, recent capital expenses, and any planned projects. The more information you provide, the more accurate the study will be.

Step 4: Review the draft report. The reserve study professional will deliver a draft report that includes the physical and financial analyses and the funding plan. Review the report carefully. Check that all components are included and that the useful life estimates make sense. If something looks wrong, ask questions.

Step 5: Adopt the funding plan. Once the final report is complete, your board should formally adopt the funding plan. This means adjusting your annual budget to include the recommended reserve contributions. If the recommended contribution exceeds your current budget, you'll need to raise fees or phase in the increase over several years.

Step 6: Communicate the plan to homeowners. Share the reserve study with your community. Explain what components are included, when major expenses are expected, and how the funding plan protects everyone from special assessments. Transparency reduces pushback when fee increases are necessary.

Step 7: Update the study annually. Work with your reserve study professional to update the financial analysis each year. This keeps your funding plan on track and allows you to adjust for unexpected expenses or changes in component condition.

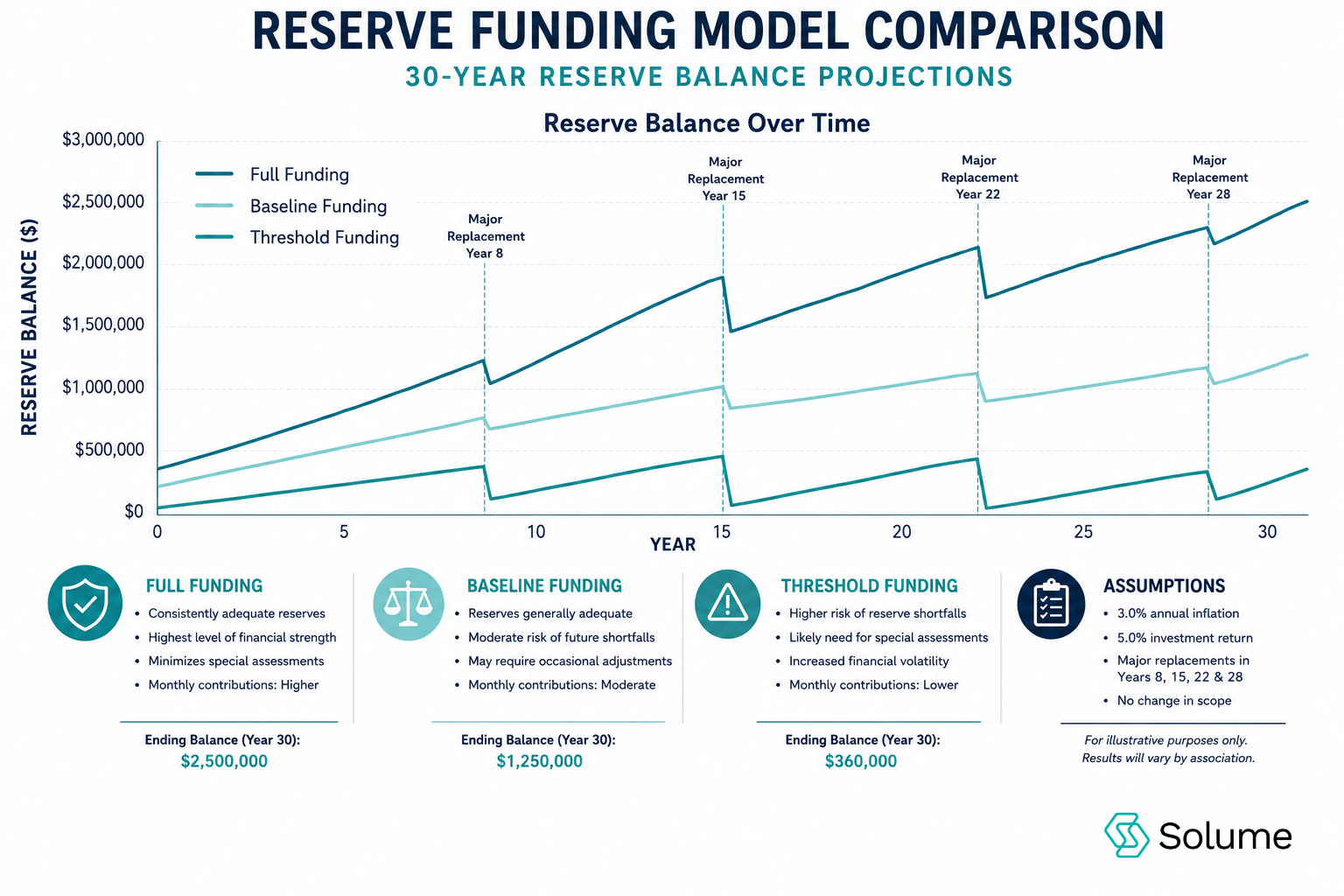

Reserve Funding Strategies and Models

Once you have a reserve study, your board needs to choose a funding strategy. There are three main models: full funding, baseline funding, and threshold funding.

Full funding means your reserve balance equals the current value of all deterioration. If your roof is halfway through its useful life, you should have half the replacement cost saved. Full funding is the gold standard. It ensures that each generation of homeowners pays for the wear and tear that occurs during their time in the community. Full funding eliminates the risk of special assessments and keeps your percent funded at or near 100%.

Baseline funding means you save just enough to cover expenses as they come due. Your reserve balance will fluctuate. It will build up before a major expense and drop to near zero after the expense is paid. Baseline funding is less expensive in the short term, but it's riskier. If an unexpected expense occurs or costs come in higher than projected, you won't have a cushion.

Threshold funding means you set a minimum reserve balance and fund just enough to stay above that threshold. This is the riskiest approach. Threshold funding often results in special assessments because the reserve balance is too low to absorb unexpected costs. Most reserve study professionals don't recommend threshold funding for South Carolina communities.

The funding strategy you choose affects how much your board contributes to reserves each year. Full funding requires higher contributions but provides the most financial stability. Baseline funding requires lower contributions but leaves less margin for error.

Most South Carolina associations should aim for full funding or baseline funding. Threshold funding is appropriate only for communities with very low capital expenses or those that plan to dissolve in the near future.

Your reserve study will show projections for all three funding models. Review the projections with your board and choose the model that balances financial responsibility with homeowner affordability.

How Self-Managed South Carolina Boards Can Track and Update Reserve Studies Without a Management Company

Many South Carolina communities are self-managed. Volunteer boards handle the finances, coordinate maintenance, and make decisions without a property management company. That doesn't mean you can't maintain a reserve study.

Self-managed boards can track and update reserve studies using basic tools. Here's how.

Start with a professional reserve study. Even if you're self-managed, hire a professional to conduct the initial study. The physical analysis and funding plan are too complex to do accurately without experience. Once you have the baseline study, you can manage updates yourself.

Track actual expenses against the reserve plan. Each time you spend money on a capital expense, compare the actual cost to the projected cost in your reserve study. If the actual cost is significantly higher or lower, adjust your future projections. This helps you refine your funding plan over time.

Update useful life estimates annually. As components age, update the remaining useful life in your reserve plan. If your reserve study says the roof has 10 years of useful life remaining, update that to 9 years the following year. If you replace a component early, update the useful life to reflect the new installation date.

Adjust for inflation. Replacement costs increase over time. Use a standard inflation rate (typically 2% to 3% per year) to adjust future replacement costs. This keeps your funding plan realistic.

Recalculate your annual contribution. Once you've updated expenses, useful life, and replacement costs, recalculate how much your board should contribute to reserves each year. If your reserve balance is lower than projected, you'll need to increase contributions. If your balance is higher, you may be able to reduce contributions or redirect funds to other priorities.

Use software designed for self-managed boards. Tracking all of this in a spreadsheet is possible, but it's tedious. Solume offers reserve study tracking built specifically for self-managed HOAs. You can upload your reserve study, track expenses, and update projections without needing a management company or a finance degree.

The key is consistency. Update your reserve plan at least once a year. The more often you review the data, the easier it is to spot problems before they become crises.

Using Reserve Study Data for Long-Term Capital Planning and Transparency

A reserve study isn't just a budget tool. It's a communication tool. The data in your reserve study helps your board make better decisions and helps homeowners understand why those decisions are necessary.

Use the reserve study to justify fee increases. When your board proposes raising fees, homeowners want to know why. The reserve study gives you a clear answer. You can show exactly which components need attention, when they'll need to be replaced, and how much it will cost. That transparency reduces resistance.

Use the reserve study to prioritize projects. Not every capital expense is equally urgent. Your reserve study shows which components are near the end of their useful life and which ones can wait. This helps your board allocate funds strategically and avoid wasting money on low-priority projects.

Use the reserve study to evaluate vendor bids. When you solicit bids for a major project, compare the bids to the replacement cost in your reserve study. If a bid comes in significantly higher, you know to ask questions or seek additional quotes. If a bid comes in lower, you can feel confident that you're getting a fair price.

Use the reserve study to educate new board members. Volunteer boards turn over frequently. New board members often don't understand the community's financial obligations. The reserve study is the fastest way to bring new members up to speed on what the association owns, what it will cost to maintain, and how the funding plan works.

Use the reserve study to build credibility with homeowners. Transparency builds trust. Share the reserve study at annual meetings, post it on your community website, and reference it in newsletters. When homeowners see that the board has a plan, they're more likely to support the board's decisions.

Use the reserve study to protect property values. Buyers and lenders review reserve studies when evaluating a community. A well-funded reserve account and a clear capital plan make your community more attractive to buyers. That protects property values for everyone.

The most successful South Carolina boards treat the reserve study as a living document for long-term planning. They review it regularly, update it annually, and use it to guide every major financial decision. Understanding HOA Reserve Study Requirements in South Carolina means recognizing that even without a state mandate, reserve planning remains the foundation of responsible board governance.

Frequently Asked Questions

Does South Carolina law require HOAs to conduct reserve studies?

No, neither the South Carolina Homeowners Association Act nor the South Carolina Horizontal Property Act requires reserve studies. Your governing documents may still require them, and federal lending guidelines often do.

How often should an HOA in South Carolina update its reserve study?

Conduct a full reserve study every three to five years and update the financial analysis annually to adjust for actual expenses and changes in your reserve balance.

Who should perform a reserve study for our HOA?

Hire a credentialed reserve study professional with experience in South Carolina communities, looking for credentials like Reserve Specialist (RS) or Professional Reserve Analyst (PRA).

Is it worth paying for a reserve study if South Carolina doesn't require one?

Yes, a reserve study protects your board from special assessments, deferred maintenance, and potential liability. The cost of a study is far less than the cost of financial surprises.

Can our HOA borrow from reserves if we plan to repay it?

Check your governing documents, as some allow temporary borrowing from reserves, but best practices discourage it because borrowing from HOA reserve funds weakens your financial position and increases the risk of special assessments.

What components should be included in our reserve study?

Include all common elements with a useful life longer than one year and a replacement cost over a threshold (typically $1,000 to $5,000), such as roofs, pavement, pools, fences, siding, and clubhouse equipment.

What happens if our board skips the reserve study and something breaks?

You'll face a special assessment or emergency borrowing, both of which are expensive and unpopular with homeowners and could have been avoided with proper reserve planning.

Is a reserve study worth it for a small HOA with only 20 homes?

Many assume small communities don't need reserve studies, but in reality, small HOAs face the same capital expenses as larger ones, with fewer homeowners to share the cost. A $30,000 roof replacement divided among 20 homes is $1,500 per household, making reserve planning even more critical for small communities.

Ready to Take Control of Your Reserve Planning?

Most South Carolina boards wait until a crisis to think about reserves. By then, the options are limited, and the costs are high.

Understanding HOA Reserve Study Requirements in South Carolina andtreating long-term planning as a board responsibility helps protect your operating and reserve funds alike. Success requires managing reserve funds responsibly and integrating reserve planning into your annual budget planning process. If your board wants a clearer way to manage finances, reserve planning, and capital expenses, Solume helps self-managed communities track reserve studies, update funding plans, and stay transparent with homeowners. The platform includes software designed for self-managed boards that simplifies financial oversight. You can explore your options with a 15-minute call to see if Solume is a good fit for your community.