KEY TAKEAWAYS

- An HOA reserve fund is a dedicated savings account separate from your operating budget, set aside specifically for major repairs, capital improvements, and unexpected expenses that are too large for routine dues to cover.

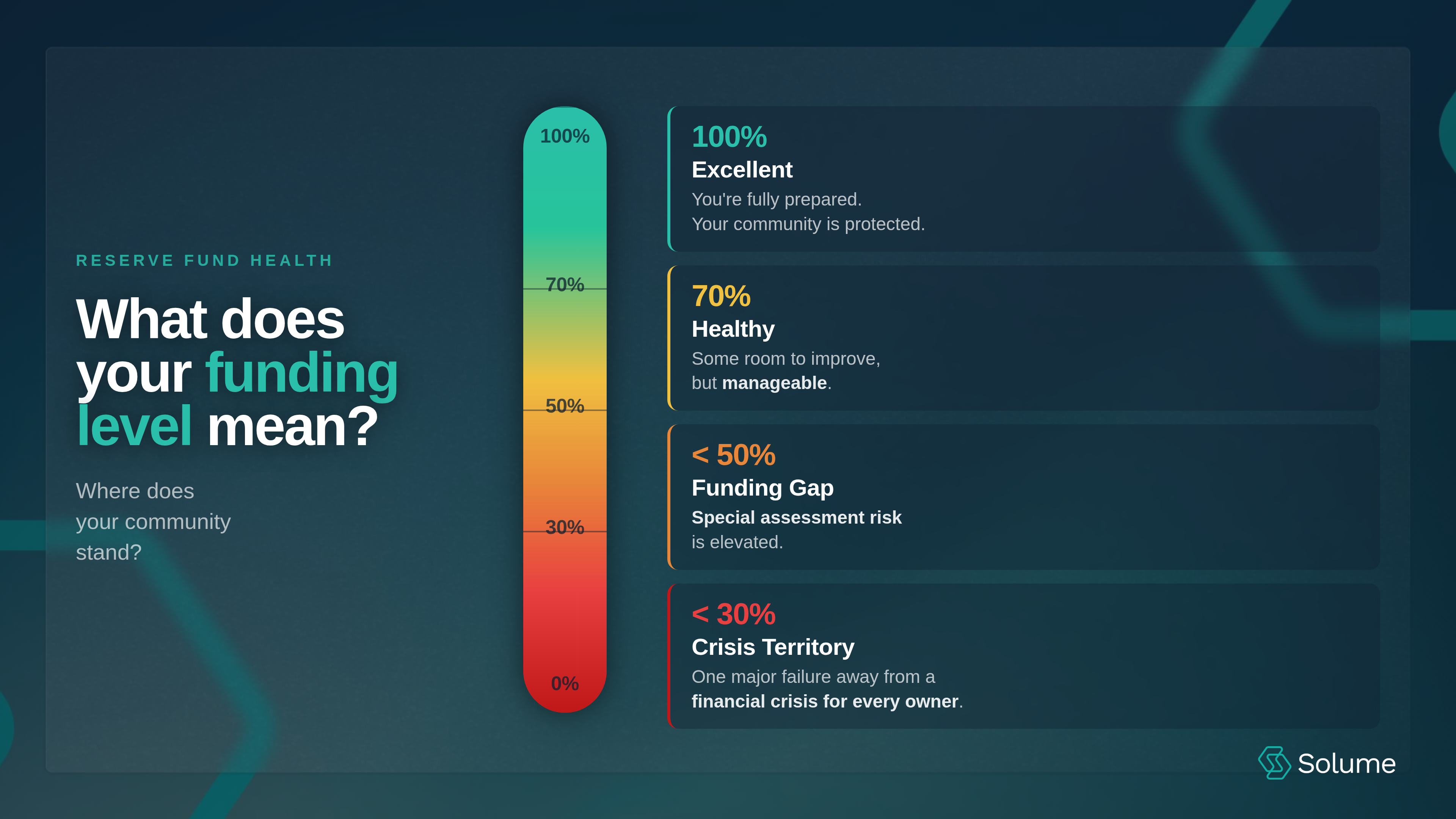

- A fully funded balance means your reserve account holds 100% of projected future costs at any given point. A fully funded balance does not mean you need all future repair costs in the bank today. Anything below 70% funded puts the community at risk of special assessments or deferred maintenance.

- Reserve funds directly protect property values. Just like a renovated home holds more value than one that hasn't been touched since it was built, a well-maintained community commands more than a neglected one.

- Professional reserve studies are not optional. They are the only reliable way to calculate how much money your HOA reserves need to hold, and they're legally required in many states.

- Fannie Mae and Freddie Mac both have reserve funding guidelines that affect whether buyers in your community can secure conventional financing. An underfunded reserve can make units nearly impossible to sell.

- Don't assume your property manager has reserve planning covered. Many don't. Reserve study management requires specific expertise that most general property management companies don't provide.

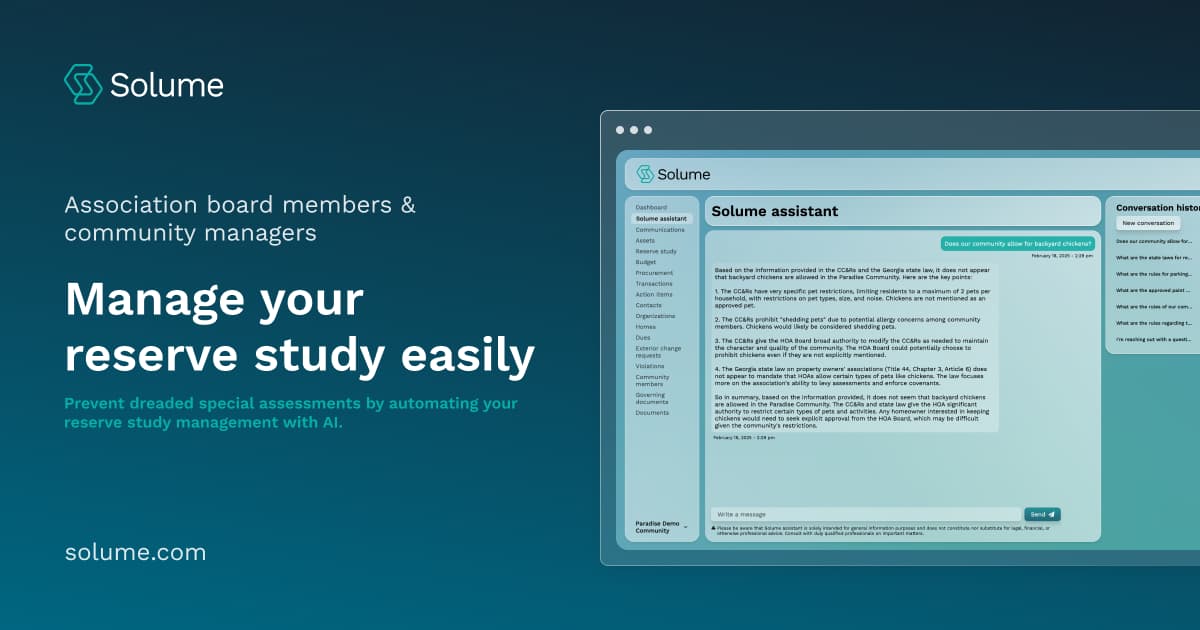

- Solume is the only all-in-one HOA management platform that includes built-in reserve study management — connecting your reserve data directly to your annual budget, board reporting, and vendor procurement.

If you've ever sat in an HOA board meeting and watched someone drop a $40,000 roof repair estimate on the table with no plan to pay for it, you already understand why HOA reserve funds exist. Or rather, why they need to be managed correctly.

Across the United States, homeowner's association reserve funds are one of the most misunderstood — and most mismanaged — aspects of community association management. Boards either underfund them, ignore them entirely, or hand the problem off to a property manager who may not be equipped to handle it. The result is predictable: emergency assessments, deferred maintenance, declining property values, and a lot of unhappy homeowners.

This guide covers everything a board member needs to know about HOA reserve funds in 2026 — what they are, how much you need, how to manage them, and how the right tools make the whole process significantly less painful.

What Is an HOA Reserve Fund and Its Intended Purpose?

Understanding the Basics

An HOA reserve fund is essentially a savings account for major repairs and replacements. It's where the money goes that's earmarked for capital expenses — the big-ticket items that come due every several years or decades. Think roof replacement on the clubhouse, resurfacing the community pool, repaving parking areas, replacing HVAC systems, or overhauling major landscaping projects. Curious about what reserve funds can be used for? Read the breakdown here.

Here's a useful way to think about it. If you were buying a home, would you rather purchase a 1970s house that looks exactly as it did when it was built, or one that's had the kitchen renovated, the roof replaced, the HVAC updated, and the windows redone? The updated home holds more value, not just aesthetically, but structurally and financially. The same logic applies to entire communities. A homeowners' association that has consistently maintained and improved its common areas holds more appeal and more value than one that has let things deteriorate. The reserve fund is what makes that sustained investment possible.

If you want to go deeper on exactly what those funds can and can't be spent on, see our full breakdown of what HOA reserve funds can be used for.

Without adequate reserves, boards are forced to make reactive decisions, patching things instead of replacing them, delaying necessary repairs, or passing emergency assessments that catch homeowners completely off guard. None of those outcomes is good for anyone.

How It Differs From Association Dues

This is a distinction that trips up a lot of new board members. Association dues fund the operating budget, the day-to-day expenses that keep the community running. That includes things like insurance premiums, landscaping maintenance contracts, utility costs for common areas, management fees, and regular cleaning services. The operating funds cover what happens every month.

Reserve funds are different. They cover what happens every ten to thirty years. Roof replacement. Pool resurfacing. Elevator modernization. Major parking lot repairs. These are not operating costs — they're capital projects, and they need to be funded separately and systematically.

Transparent communication with homeowners about how both pools of money work is essential. When residents understand why reserve contributions show up in their dues and what those funds are protecting them from, they're far more likely to support increases when needed rather than treating every budget discussion like a fight.

Key Components of HOA Reserve Fund Planning

The Role of Reserve Studies

You can't know how much money to set aside if you don't know what you own, what condition it's in, and how long it has left before it needs to be replaced. That's exactly what a professional reserve study provides.

A reserve study is a formal assessment of your community's major assets. A credentialed reserve specialist conducts an on-site inspection to evaluate the useful life and current condition of every significant component the HOA maintains — the clubhouse roof, the swimming pool, the parking structure, HVAC systems, fencing, lighting, and everything else. That physical analysis is then paired with a financial analysis that calculates the replacement costs over time and determines the annual reserve contributions required to fund them.

The resulting funding plan is the foundation of sound HOA finances. Without it, reserve planning is guesswork. With it, boards have a defensible, data-driven basis for every financial decision related to the community's long-term assets. Regular reviews — at minimum every three to five years, with annual internal check-ins — keep the funding plan aligned with the association's actual needs as costs change and assets age. For a deeper look at how often that plan should be revisited, see our guide on how often you should update a reserve study.

The HOA reserve study is also the document lenders, buyers, and state regulators will ask for — so keeping it current protects the association on multiple fronts.

Funding Requirements and Strategies

The rule of thumb in the industry is to target a fully funded balance. A fully funded balance means your reserve account holds 100% of the money that has theoretically been "used up" by wear and tear on your community's assets to date. Think of it this way: if a roof has a 20-year lifespan and is 10 years old, a fully funded reserve account holds 50% of that roof's replacement cost set aside and ready. Across every asset the association maintains, a fully funded balance means you're never caught without the money to handle what's coming.

In practice, most associations don't hit 100%. The widely accepted minimum is 70% funded. Anything below that and you're in territory where a single large repair or a string of smaller ones can trigger an emergency assessment or require a lump sum contribution that no one budgeted for.

Fannie Mae and Freddie Mac both have guidelines around reserve funding levels, and lenders pay attention. If your community's reserves are inadequate, buyers may be unable to secure conventional financing for units in your association. That's not a theoretical risk — it's a real dynamic that's made units harder to sell in communities that let their reserves slip. Freddie Mac's requirements in particular have become more stringent in recent years following high-profile structural failures in condominium communities.

On the contribution side, boards generally have two strategies: steady annual reserve contributions built into regular dues, or periodic lump sum contributions when gaps develop. Incremental annual contributions are almost always the better path — they're more predictable for homeowners, easier to budget for, and less likely to create political resistance than a sudden large assessment.

How Much Money Should Be in an HOA's Reserve Fund?

Determining Adequate Reserves

There's no universal dollar amount that applies to every community, and anyone who tells you otherwise is guessing. The right answer depends entirely on what your community owns, how old those assets are, what it costs to replace them, and what your state requires.

Size matters in obvious ways. A 500-unit high-rise condominium with elevators, a parking structure, a swimming pool, fitness facilities, and a full roofing system has dramatically different reserve needs than a 40-home planned community with a modest clubhouse and a parking lot. The estimated cost of each capital component — roof replacement, pool resurfacing, HVAC systems, and major landscaping projects — needs to be individually evaluated and projected forward.

State law adds another layer. California Civil Code has specific reserve study and funding requirements for HOAs. Florida has enacted its own legislation in the wake of the Surfside condominium collapse, with mandatory reserve requirements for condominium associations. If you operate in a state with reserve requirements, compliance isn't optional — and the penalties for non-compliance go beyond financial exposure. They can affect board members personally.

The bottom line: a professional HOA reserve study is the only way to arrive at an accurate, defensible funding target for your specific community — and in many states, it's legally required.

Maintaining Financial Health

Once you know your funding target, the next question is where to hold the money. Reserve fund money should be in secure deposit accounts — FDIC-insured vehicles like money market accounts, certificates of deposit, or laddered CD strategies that balance liquidity with favorable interest rates. The goal isn't to generate aggressive returns; it's to preserve capital, maintain liquidity for upcoming projects, and earn enough interest to partially offset inflation. Leaving reserve fund money in a low-yield basic bank account is a missed opportunity, but chasing returns in speculative investments is a fiduciary risk.

Percent funded tracking is something boards should review at least annually. Your reserve study provider can update this calculation based on your current reserve balance and any changes to replacement cost estimates. A community that was 75% funded three years ago may now be at 60% if contributions haven't kept pace with inflation and asset aging.

Here's something worth saying directly: don't assume your property manager or HOA management company has this covered. Many general property management companies are excellent at handling day-to-day operations — they're not necessarily equipped to manage reserve studies or financial planning at the level this requires. Reserve study management is a specialized discipline. No one is going to care about your community's long-term financial health as much as your board does. Verify that whoever is handling your reserves actually understands what they're doing, and don't outsource the oversight.

Best Practices for HOA Reserve Fund Management

After working with communities across the country, a few practices consistently separate well-run associations from ones that end up in crisis.

- Partner with the Community Associations Institute. CAI is the leading national organization for HOA governance, and their resources on reserve planning, board education, and industry standards are genuinely useful. If you're not familiar with them, start there.

- Make reserve needs a line item in the operating budget reviewed on a regular basis. Reserve contributions should never be an afterthought. They belong in the budget from day one, reviewed annually, and adjusted whenever a reserve study update indicates a gap.

- Build funding strategies that account for unexpected costs and emergency repairs. Even a well-funded reserve can get hit by a storm, a structural failure, or a sudden equipment breakdown. Your funding plan should include a buffer for genuine emergencies.

- Develop an investment strategy for your reserve fund money. Work with a financial advisor or CPA who understands community association finances to identify the right deposit accounts and CD ladder structure for your current balance and upcoming project timeline.

- Give homeowners portal access to reserve fund reports. Transparent communication isn't just good governance — it's the difference between homeowners who trust the board and homeowners who show up to meetings ready to fight. When residents can see the data, suspicion goes down, and cooperation goes up.

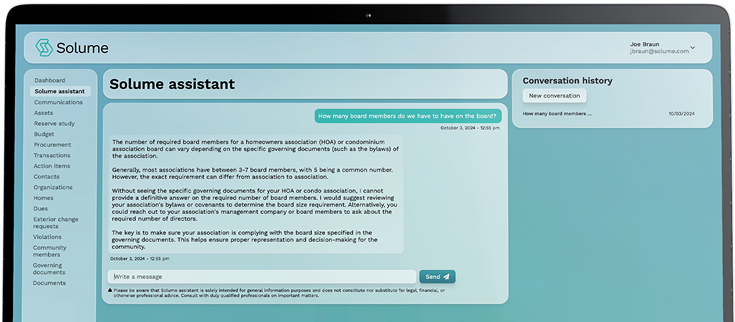

Solume is the only all-in-one HOA management platform that includes built-in reserve study management. Most HOA software handles communications, dues collection, and violation tracking — and then leaves boards on their own when it comes to the financial planning work that actually protects the community. Solume was built differently. Reserve study data lives in the same platform as your annual budget, your vendor procurement, your board reporting, and your homeowner communications. That integration means reserve planning isn't an isolated task that gets handled once every few years and forgotten. It's a living part of how your community operates — visible, trackable, and connected to everything else. And it's built to be genuinely user-friendly for volunteer board members, not just financial professionals.

How HOA Reserve Funds Impact Property Management

Protecting Community Assets

A well-funded reserve is one of the most powerful tools a board has for protecting the long-term value of the community. When the money is there, repairs happen on schedule. Deferred maintenance doesn't compound. The community stays attractive to buyers. And homeowners aren't blindsided by emergency assessments that strain household budgets and create resentment.

The alternative plays out predictably. An underfunded reserve leads to deferred repairs. Deferred repairs lead to deterioration. Deterioration affects property values. And when a major failure finally forces action, the board faces a choice between a large special assessment, an emergency assessment for immediate costs, or taking on debt — none of which anyone wants. Proactive financial planning isn't just responsible governance; it's what keeps the association's members from bearing the full weight of neglect all at once.

Special assessments, when they do occur, are often a symptom of inadequate reserve planning rather than unavoidable circumstances. Some are genuinely unavoidable — disaster damage, unforeseen structural failures, costs that exceed any reasonable projection. But the majority of special assessments in the United States trace back to associations that knew repairs were coming and didn't fund for them adequately.

Working With a Reserve Analyst or Specialist

The reserve analyst is one of the most important outside professionals your association works with, and they don't always get treated that way. A qualified reserve analyst does far more than produce a report — they help the board understand the estimated cost and timing of every major capital project, develop realistic funding strategies, ensure compliance with the association's governing documents, and provide the documented basis for reserve contributions that protects board members from liability claims.

Look for designations from the Association of Professional Reserve Analysts (APRA) or the Community Associations Institute's Reserve Specialist (RS) credential. Ask for references from communities similar in size and type to yours. And build a relationship with your analyst that goes beyond the three-to-five year study cycle — your reserve fund study should be a living document, not a binder that sits on a shelf.

Ensuring the Longevity of HOA Reserve Funds in 2026

The communities that manage their reserves well over the long term share a few common traits. Their boards treat reserve planning as a year-round responsibility, not an annual budget line item. They engage consistently with homeowners about the financial health of the community, building the trust that makes necessary contribution increases easier to pass. They work with qualified reserve analysts and update their studies regularly. And they use tools that keep reserve data connected to every other aspect of community management.

As funding requirements tighten nationally — driven by legislation responding to structural failures, changing lender guidelines from Fannie Mae and Freddie Mac, and growing awareness of the consequences of underfunding — the bar for what constitutes adequate reserve management is only going up. Boards that get ahead of that curve protect their communities, their homeowners, and themselves. Those that don't will eventually face the consequences that every underfunded reserve account eventually produces.

The good news is that the path forward is straightforward: know what you own, know what it costs to maintain it, fund it consistently, and use tools that make the whole process manageable. Start there, and the rest follows.

Ready to see how Solume handles reserve study management alongside everything else your board needs? A 15-minute call is enough to know whether it's the right fit.

Frequently Asked Questions: HOA Reserve Funds

1. What is an HOA reserve fund?

An HOA reserve fund is a dedicated savings account separate from the operating budget, used exclusively for major repairs, replacements, and capital improvements to common areas — things like roof replacement, parking lot resurfacing, pool equipment, and HVAC systems. It's the financial safety net that keeps the community from being blindsided by large, predictable expenses.

2. How much money should an HOA have in reserves?

It depends entirely on your community — its size, the age and condition of its assets, and what it costs to replace them. The industry rule of thumb is to maintain a fully funded balance of 100%, with 70% as the minimum acceptable threshold. Anything below 70% puts the community at meaningful risk of special assessments. The only reliable way to determine the right number for your community is a professional reserve study.

3. What's the difference between HOA reserves and operating funds?

Operating funds cover day-to-day expenses: management fees, insurance premiums, landscaping contracts, utilities for common areas, and routine maintenance. Reserve funds cover capital projects that happen every several years or decades — roof replacements, pool resurfacing, and major structural repairs. They're funded separately and should never be commingled.

4. What happens if an HOA's reserve fund is underfunded?

The board faces an ugly set of options: levy a special assessment on homeowners, take out a loan, defer the repair (which makes it more expensive later), or do a combination of all three. Beyond the immediate financial pain, an underfunded reserve can affect lender approval for buyers, making units harder to sell and suppressing property values across the entire community.

5. Are HOA reserve funds legally required?

In many states, yes. Reserve studies and adequate reserve funding are legally required for condominium associations in states including California, Florida, Nevada, New Jersey, Hawaii, and others. Even where state law doesn't mandate it, most governing documents require adequate reserves, and board members can face personal liability for failing to fund them appropriately.

6. What is a fully funded balance?

A fully funded balance means your reserve account holds 100% of the money that has theoretically been consumed by the useful life of your community's assets to date. If a parking lot has a 20-year lifespan and is 10 years old, a fully funded reserve holds 50% of the replacement cost set aside. Across every asset, it means you're never caught short when a replacement comes due.

A fully funded balance does not mean you need all future repair costs in the bank today. It means your reserve balance matches the portion of your assets' useful life that has already been consumed. If a $100,000 roof is halfway through its 20-year lifespan, a fully funded reserve holds $50,000 toward it — today. Apply that logic across every asset the association owns to get your current funding target.

7. How do Fannie Mae and Freddie Mac affect HOA reserve requirements?

Both agencies have guidelines requiring adequate reserve funding for conventional mortgage approval in condominium communities. If a community's reserves are deemed inadequate, buyers may be unable to secure conventional financing, which directly affects unit saleability and market value. Following high-profile structural failures, these requirements have become more stringent, and lenders are checking more carefully.

8. How often should an HOA conduct a reserve fund study?

A full HOA reserve study with a site inspection should be done at a minimum every three to five years. Most states that require reserve studies mandate updates on a similar schedule — California requires a review every three years. Annual internal reviews are also recommended to track your percent funded status and catch gaps before they become crises. Associations that update annually consistently see lower rates of special assessments.

9. Can the HOA board manage reserve planning without a professional?

Technically possible in some states — practically inadvisable. Most lenders won't accept a self-conducted study for mortgage approval purposes, and a board that gets the numbers wrong carries real fiduciary risk. A credentialed reserve analyst brings construction cost databases, depreciation standards, and liability coverage. The cost of a professional reserve study is trivial compared to the cost of an underfunded reserve.

10. What should we look for in an HOA management company for reserve planning?

Most general HOA management companies handle operations well — they're not always equipped for reserve study management. Look specifically for a company or platform that integrates reserve study management with the rest of your HOA finances, not one that treats it as an add-on. Ask directly: do they manage the reserve study process, update funding projections annually, and connect reserve data to the operating budget? If the answer is vague, keep looking. Solume was built specifically to close this gap.