Most HOA boards in Pennsylvania assume they're off the hook because the state doesn't require reserve studies. That assumption costs communities thousands of dollars in emergency special assessments every year.

Here's the hard truth: just because Pennsylvania doesn't mandate a reserve study doesn't mean your board can skip capital planning. Pennsylvania boards still operate under fiduciary duties outlined in the Uniform Condominium Act and Uniform Planned Community Act. Those duties include managing reserve funds responsibly and disclosing financial conditions to homeowners.

Without a reserve study, boards are guessing. They're estimating roof lifespans, pavement costs, and HVAC replacement costs based on gut instinct rather than data. That approach works until it doesn't, and once a $200,000 roof replacement comes due with no reserve fund to cover it, homeowners pay the price through special assessments.

This guide explains Pennsylvania's statutory framework, why reserve studies still matter in non-mandate states, and how Pennsylvania communities can avoid financial surprises through proactive reserve planning. For an overview of reserve study requirements across all 50 states, boards can compare Pennsylvania's approach with those of more prescriptive jurisdictions.

Key Takeaways

- Pennsylvania HOA reserve study requirements are not mandated by state law for most associations, but the Uniform Condominium Act and Uniform Planned Community Act require reserve fund disclosure and impose fiduciary duties on boards that make reserve studies essential.

- Pennsylvania boards operate under the prudent investor rule, which creates a legal expectation of responsible long-term planning even in the absence of explicit reserve study requirements.

- Reserve studies protect communities from special assessments, deferred maintenance, and declining property values by identifying future capital needs before they become emergencies.

- Lenders like Fannie Mae and FHA often require reserve studies for mortgage approval, making them essential even in states without legal mandates.

- Self-managed HOAs in Pennsylvania benefit significantly from reserve studies because volunteer boards rarely have the financial expertise to forecast major repairs without professional guidance.

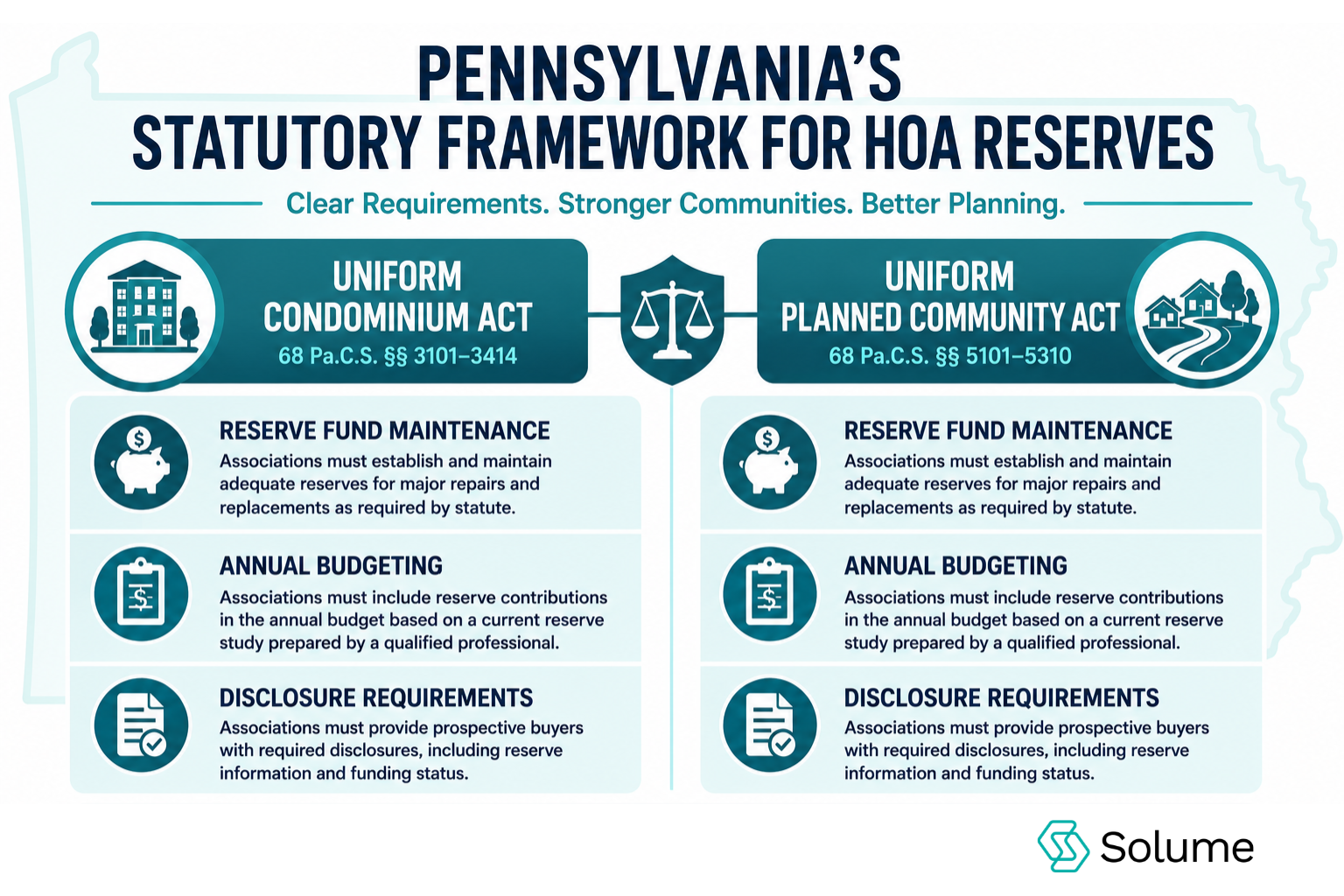

Pennsylvania Statutory Framework: Uniform Condominium Act and Uniform Planned Community Act

Pennsylvania regulates condominiums under the Uniform Condominium Act (68 Pa.C.S. §§ 3101-3414) and planned communities under the Uniform Planned Community Act (68 Pa.C.S. §§ 5101-5414). Neither statute requires reserve studies, but both impose financial responsibilities on boards, making reserve planning a practical necessity.

The Uniform Condominium Act requires condominium associations to maintain a reserve fund for capital expenditures and deferred maintenance. Section 3315(a)(7) mandates that boards prepare annual budgets that include "reasonable reserves" for repair and replacement of common elements.

The Uniform Planned Community Act contains similar language. Section 5315(a)(7) requires planned community associations to budget for reserves, though it doesn't specify how much or how boards should calculate those amounts. These statutes are maintained and updated by the Pennsylvania General Assembly, which oversees all state legislation affecting community associations.

Both statutes also require reserve fund disclosure. Pennsylvania boards must provide homeowners with annual financial statements that include the current balance of the reserve fund and a summary of how those funds are allocated.

What many communities don't realize is that these disclosure requirements create indirect pressure to implement reserve studies. If your board tells homeowners the reserve fund has $50,000 but can't explain whether that's enough to cover the next roof replacement, you're inviting questions you can't answer.

Board Fiduciary Duty and the Prudent Investor Rule in Pennsylvania

Pennsylvania boards operate under fiduciary duties that go beyond the statutory minimums set forth in the Uniform Condominium Act and the Uniform Planned Community Act. These duties come from common law and apply to anyone managing other people's money.

The prudent investor rule requires board members to manage association funds with the care, skill, and caution that a prudent person would use. In practice, this means Pennsylvania boards can't ignore long-term planning just because the state doesn't mandate reserve studies.

Courts in other states have held boards liable for failing to adequately fund reserves, even when state law didn't require reserve studies. The reasoning is simple: a prudent person wouldn't let a roof deteriorate to the point of failure without setting aside money for replacement.

The risk most boards overlook is that fiduciary duty claims often come from homeowners, not regulators. If your board skips reserve planning and then levies a $10,000 special assessment on each unit, expect homeowners to ask why the board didn't plan ahead.

The prudent investor rule doesn't require perfection, but it does require effort. Pennsylvania boards that commission reserve studies and follow their recommendations have a much stronger defense if homeowners later challenge those financial decisions.

Best Practices for Reserve Studies in Non-Mandate States

Pennsylvania communities should treat reserve studies as best practices even though they're not legally required. The goal is to avoid the financial instability caused by reactive maintenance and emergency special assessments.

Best practices for Pennsylvania HOA boards include commissioning a full reserve study every three to five years. A full reserve study includes both a physical analysis and a financial analysis. The physical analysis involves a site visit to inspect all reserve components, including roofs, pavement, siding, HVAC systems, and other common elements. The financial analysis projects the cost of repairing or replacing those components and calculates how much the community should contribute to the reserve fund each year.

Between full reserve studies, Pennsylvania boards should update their reserve study annually. A reserve study update adjusts the financial analysis for inflation, changes in interest rates, and any unexpected repairs that occurred during the year.

Pennsylvania boards should also establish a reserve funding goal. The three most common goals are full funding, threshold funding, and baseline funding. Full funding means the reserve fund always has enough money to cover the deterioration that's already occurred. Threshold funding targets a specific percent-funded metric, such as 70%. Baseline funding aims to keep the reserve fund balance above zero.

Pennsylvania boards should also integrate reserve planning into their annual budget process. The reserve study should drive the reserve contribution, not the other way around. Organizations like the Community Associations Institute provide educational resources to help boards implement these best practices effectively.

Benefits of Reserve Studies

Avoiding Special Assessments and Financial Stability

Special assessments are the most visible consequence of poor reserve planning. A board in a 50-unit Pennsylvania condo community discovered this the hard way after postponing roof repairs for three years to avoid raising fees. By the time the roof failed during a winter storm, emergency repairs cost $180,000, and the reserve fund held only $22,000. The board levied a $3,160 special assessment per unit, payable within 60 days, triggering multiple owner lawsuits and three board resignations.

A reserve study prevents special assessments by identifying future capital needs and spreading the cost over time. Instead of asking homeowners to pay $10,000 each time the roof fails, the board collects smaller amounts each year and builds a reserve fund large enough to cover the replacement cost when needed. Boards looking for strategies to avoid surprise special assessments will find that proactive reserve planning is the most effective approach.

Financial stability is the broader benefit. Communities with adequate reserve funds can handle unexpected repairs without financial panic.

Reserve studies also reduce the risk of deferred maintenance. Boards that don't have a reserve study often delay repairs because they don't have the money. That deferred maintenance compounds over time.

Protecting Property Values

Property values in HOA and condo communities depend heavily on the condition of common elements. Buyers notice cracked pavement, aging roofs, and deferred maintenance. Those visible problems signal financial instability, and buyers either walk away or demand lower prices.

A reserve study protects property values by ensuring the community maintains its common elements. Buyers see a well-maintained community with a funded reserve study and gain confidence that the HOA won't hit them with a special assessment six months after closing.

Real estate agents also ask about reserve funds during the sales process. If your Pennsylvania condo association can't provide a reserve study or show a healthy reserve fund balance, agents will warn their buyers.

According to the Community Associations Institute, communities with deferred maintenance and low reserve funds sell for 5% to 15% less than comparable communities with strong reserves. For a $300,000 condo, that's a $15,000 to $45,000 loss per unit.

Meeting Lender Requirements (Fannie Mae, FHA)

Fannie Mae and FHA both require reserve studies for mortgage approval in many HOA and condo communities. If your Pennsylvania community doesn't have a reserve study, buyers who need financing may not be able to close.

Fannie Mae's condo project approval standards require condo projects to maintain adequate reserves for capital expenditures and deferred maintenance. Lenders interpret "adequate reserves" by reviewing the community's reserve study and reserve fund balance. If the reserve study shows the community is less than 10% funded, Fannie Mae may reject the project for financing.

FHA has similar requirements. FHA-approved condos must demonstrate financial stability, and the reserve study is the primary tool FHA uses to assess that stability. FHA also requires that at least 10% of the annual budget be allocated to reserves.

Pennsylvania communities that don't meet Fannie Mae or FHA requirements lose access to a large pool of buyers. Most first-time homebuyers rely on FHA loans, and many repeat buyers use conventional loans backed by Fannie Mae.

Pennsylvania boards that want to maintain strong resale values should commission a reserve study and ensure the community meets Fannie Mae and FHA lender requirements.

What Is a Reserve Study: Physical Analysis and Financial Analysis Components

A reserve study has two main components: a physical analysis and a financial analysis. Both are necessary to create an accurate long-term capital plan. Boards unfamiliar with the process can review what a reserve study actually includes to understand the full scope of the assessment.

The physical analysis starts with a site visit. A reserve study professional inspects all reserve components, including roofs, pavement, siding, decks, pools, HVAC systems, elevators, and other common elements. The goal is to assess the current condition of each component and estimate its remaining useful life.

For example, if your Pennsylvania community has an asphalt parking lot installed 15 years ago, the reserve study professional will inspect the pavement for cracks, potholes, and other deterioration. Based on that inspection, they'll estimate how many more years the pavement will last before it needs resurfacing or replacement.

The financial analysis uses data from the physical analysis to develop a funding plan. It calculates how much money the community should contribute to the reserve fund each year to cover future repairs and replacements. The financial analysis also projects the reserve fund balance over time, indicating when major expenditures will occur and whether the fund will have sufficient funds to cover them.

The financial analysis typically includes three funding scenarios: full funding, threshold funding, and baseline funding. Each scenario shows a different reserve contribution and a different projected reserve fund balance.

How to Read a Reserve Study: Percent Funded Metric

The percent funded metric is the single most important number in a reserve study. It tells you whether your reserve fund is healthy or at risk.

Percent funded is calculated by dividing the current reserve fund balance by the fully funded balance. The fully funded balance is the amount of money the reserve fund should have if the community had been funding reserves perfectly since day one.

For example, if your Pennsylvania condo association has $200,000 in the reserve fund and the fully funded balance is $500,000, your percent funded is 40%. That means the reserve fund has 40% of the money it should have.

Most reserve study professionals use the following benchmarks to interpret percent funded:

- 70% to 100%: Strong reserves. The community is well-positioned to handle future capital expenditures without special assessments.

- 30% to 70%: Fair reserves. The community is underfunded but not in immediate crisis. The board should increase reserve contributions to avoid future special assessments.

- 0% to 30%: Weak reserves. The community is significantly underfunded and at high risk for special assessments or deferred maintenance.

Pennsylvania boards should aim for at least 70% funded. Communities with less than 30% funding should treat reserve planning as an urgent priority.

Percent funded also matters to lenders. Fannie Mae and FHA both use percent funded to assess financial stability.

Reserve Funding Goals: Full Funding vs Threshold vs Baseline

Pennsylvania boards need to choose a reserve funding goal, which determines how much the community contributes to reserves each year.

Full funding means the reserve fund always has enough money to cover the deterioration that's already occurred. If your roof is halfway through its useful life, the reserve fund should have half the replacement cost saved. Full funding keeps the percent funded metric at or near 100% at all times.

Full funding is the most conservative approach and the best protection against special assessments. It's also the most expensive because it requires higher reserve contributions, especially for underfunded communities trying to catch up.

Threshold funding targets a specific percent-funded metric, such as 70% or 50%. The board sets a threshold and adjusts reserve contributions to maintain that level. Threshold funding is less expensive than full funding but still provides a meaningful cushion against unexpected repairs.

Most Pennsylvania communities should target a threshold funding level of 70% or higher. This approach balances financial stability with affordability.

Baseline funding aims to keep the reserve fund balance above zero. The board contributes just enough to cover upcoming expenses without building long-term reserves. Baseline funding is the least expensive approach, but it's also the riskiest.

Baseline-funded communities have no margin for error. If a major repair costs more than expected or occurs earlier than projected, the reserve fund becomes negative, and the board must levy a special assessment.

Pennsylvania boards should avoid baseline funding unless the community is financially distressed and has no other option.

How Pennsylvania's Framework Impacts HOAs, Condos, and Co-Ops Differently

Pennsylvania's statutory framework treats HOAs, condos, and co-ops differently, and those differences affect reserve planning.

Condominiums are subject to the Uniform Condominium Act, which explicitly requires reserve funds and reserve fund disclosures. Pennsylvania condo boards have a clear legal obligation to maintain reserves, even though the statute doesn't mandate reserve studies. The Uniform Condominium Act also gives condo boards greater authority to increase reserve contributions without homeowner approval, making it easier to implement reserve study recommendations.

Planned communities (HOAs) fall under the Uniform Planned Community Act, which has similar reserve fund requirements but slightly less prescriptive language. Pennsylvania HOA boards have the same practical need for reserve studies, but the legal framework is marginally less strict than for condos.

Co-ops are the outliers. Pennsylvania co-ops are typically governed by corporate law rather than the Uniform Condominium Act or Uniform Planned Community Act. Co-op boards still have fiduciary duties under common law, but they don't face the same statutory reserve fund requirements.

That said, Pennsylvania co-ops still benefit from reserve studies. Co-op shareholders expect the same financial stability as condo owners, and lenders apply the same reserve fund requirements to co-ops as they do to condos.

Case Study: Pennsylvania HOA That Avoided Special Assessment Through Proactive Reserve Planning

A 120-unit planned community in suburban Philadelphia commissioned its first full reserve study in 2018. The reserve study revealed the community was only 25% funded, with major expenses looming over the next five years, including a $180,000 roof replacement and a $95,000 pavement resurfacing project.

The board faced a choice: continue with minimal reserve contributions and levy special assessments once the projects came due, or increase reserve contributions immediately and avoid the assessments.

The board chose the proactive approach. They increased monthly reserve contributions by $40 per unit and communicated the reserve study findings to homeowners. The presentation included a clear comparison: pay an extra $40 per month now, or pay a $5,000 special assessment in three years once the roof failed.

Homeowners supported the increase. By 2023, the reserve fund had grown to $420,000, and the community completed both the roof replacement and pavement resurfacing without a special assessment.

The community's percent funded metric improved from 25% to 68% over five years. Property values remained stable, and the community had no difficulty meeting Fannie Mae lender requirements during the sales process.

Pennsylvania Reserve Study Requirements for Self-Managed Boards

Self-managed HOAs in Pennsylvania face unique challenges regarding reserve planning. Volunteer boards rarely have the financial expertise to forecast capital expenditures accurately, and they often underestimate the cost and complexity of major repairs.

A reserve study provides the professional guidance self-managed boards need. The reserve study professional brings expertise in building systems, cost estimating, and financial planning that most volunteer board members don't have. Boards seeking detailed guidance can follow a step-by-step guide to conducting their reserve study to ensure they capture all necessary components.

Self-managed HOAs should commission a full reserve study every three to five years and update the study annually. The reserve study update process is simple and doesn't require a site visit, which keeps costs manageable for communities with limited budgets.

Pennsylvania boards should also look for reserve study professionals with experience in their region. Local professionals understand Pennsylvania construction costs, climate conditions, and the typical lifespan of building components in the state.

Self-managed boards should integrate the reserve study into their annual budget process. The reserve study should determine the reserve contribution, not the board's guess about what homeowners will tolerate.

Finally, volunteer board members should use the reserve study as a communication tool. Homeowners trust data more than they trust the board's opinion.

Solume offers software designed for self-managed Pennsylvania communities, including reserve study integration and financial planning features that help volunteer boards manage long-term capital planning without the overhead of a professional management company.

Understanding Pennsylvania HOA Reserve Study Requirements: Operating Fund vs Reserve Fund

Many Pennsylvania boards confuse the operating fund with the reserve fund, but understanding the distinction is critical for proper financial planning. The operating fund covers day-to-day expenses like landscaping, utilities, and routine maintenance. The reserve fund, by contrast, is dedicated to major repairs and capital replacements identified in your reserve study. Understanding the difference between operating and reserve accounts helps boards allocate funds appropriately and maintain financial transparency.

Pennsylvania lenders often examine how boards separate these two funds. Commingling operating and reserve funds creates accounting problems and makes it difficult to track whether your community is adequately funded for future capital needs.

A resale certificate provides buyers with essential financial information about the community, including reserve fund status, pending special assessments, and outstanding violations. Buyers and their lenders scrutinize the resale certificate to assess financial health. If your resale certificate shows a weak reserve fund or reveals that the community lacks a reserve study, buyers may walk away or demand price concessions.

Pennsylvania boards should ensure their resale certificate accurately reflects reserve fund status and includes a summary of the most recent reserve study. This transparency protects both the seller and the buyer and demonstrates that the board is meeting its fiduciary duty to maintain adequate reserves.

Ready to take control of your community's financial future?

If your Pennsylvania board wants a clearer way to manage finances, reserve planning, and long-term capital needs, explore your options to see if Solume is a good fit for your community. Solume integrates reserve study data directly into your financial planning tools, giving self-managed boards the transparency and control they need without the overhead of a full management company.

Frequently Asked Questions

Does Pennsylvania law require HOAs to conduct reserve studies?

No, Pennsylvania does not require reserve studies for most HOAs, but the Uniform Condominium Act and Uniform Planned Community Act require reserve funds and impose fiduciary duties, making reserve planning a practical necessity.

How is Pennsylvania different from states like Florida or California regarding reserve studies?

Pennsylvania does not mandate reserve studies, while Florida and California have explicit requirements for most condos and HOAs. Pennsylvania boards still need reserve studies to meet fiduciary obligations, avoid special assessments, and satisfy lender requirements.

How often should an HOA in Pennsylvania update its reserve study?

Pennsylvania communities should commission a full reserve study every three to five years and update it annually to account for inflation, interest rates, and unexpected repairs.

What's the difference between a reserve study and a reserve fund?

A reserve study is a planning document that projects future capital needs and recommends funding levels, while a reserve fund is the actual bank account where the community saves money to pay for those future expenses. Boards can review the difference between operating and reserve accounts for detailed guidance on proper fund separation.

Is a reserve study really worth it if Pennsylvania doesn't require one?

Yes, because reserve studies prevent special assessments, protect property values, and help communities meet Fannie Mae and FHA requirements. The cost of a reserve study is far less than the financial damage caused by poor capital planning.

What happens if my Pennsylvania community skips reserve planning entirely?

Your board risks violating fiduciary duties, facing special assessments for emergency repairs, losing buyer financing options, and watching property values decline due to visible deferred maintenance.