A leaking clubhouse roof, a $9,000 estimate, and a reserve fund holding $2,300. That is the situation one volunteer treasurer in a Monmouth County condo association walked into last winter. It is the exact scenario a New Jersey HOA reserve study exists to prevent. The state now requires most community associations to plan for these big-ticket repairs years in advance. The boards that treat it as a paperwork chore tend to be the ones hit with surprise special assessments. This guide walks you through what the law requires, who must comply, and how to keep your community out of the leaking-roof position.

Key Takeaways

- A New Jersey HOA reserve study is now a legal requirement for condominiums, cooperatives, and planned developments with common area capital assets exceeding $25,000.

- The study must be updated at least every five years and prepared by a credentialed Reserve Specialist, licensed engineer, or architect, in accordance with CAI's National Reserve Study Standards.

- Every compliant reserve study includes a 30-year funding plan built to avoid special assessments and emergency loans.

- Ignoring the requirement exposes boards to legal liability, homeowner distrust, and the financial risk that deferred maintenance eventually creates.

What a New Jersey HOA reserve study is and its two components (physical and financial analysis)

A New Jersey HOA reserve study is two things stapled together: a physical analysis and a financial analysis. The physical analysis is the walkthrough. A qualified professional inventories your common area capital assets: roofs, siding, paving, elevators, pools, and retaining walls. Then they estimate the remaining useful life and cost of each one. This is where life cycle analysis lives. How many years before that 20-year roof needs replacing, and what will it cost when it does?

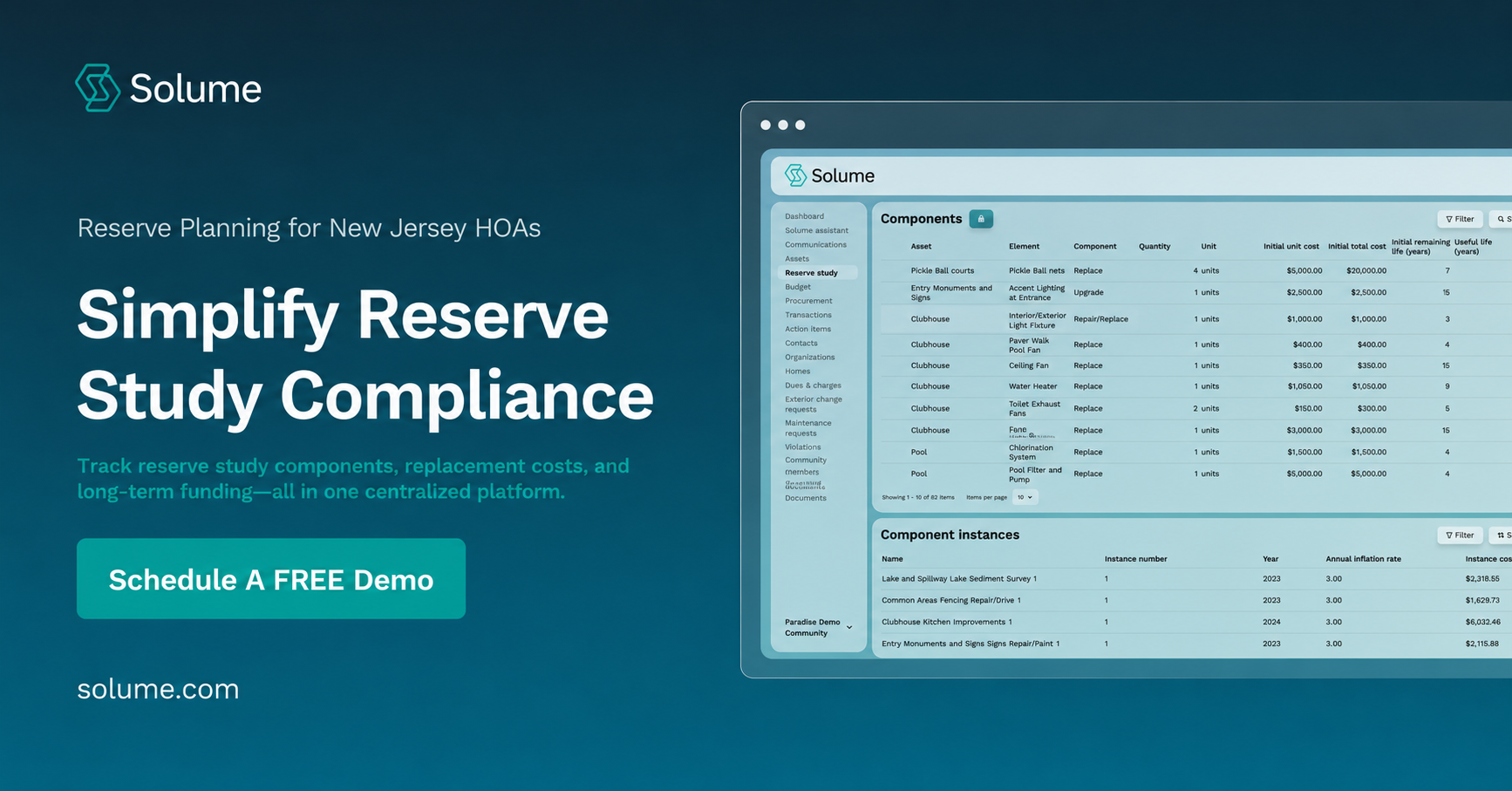

The financial analysis takes that inventory and builds a funding plan around it. It compares your current reserve funds against what you will need over the next 30 years. Then it maps the annual contributions to close any gap. This supports long-term planning because repair costs do not arrive evenly. A roof and a repaving project might both come due in year eight. Without a plan, that year becomes a special assessment. Modern automated reserve study tools can model these scenarios so boards see the funding gaps before they turn into emergencies.

Both components follow CAI's National Reserve Study Standards. Many boards assume that a bank statement showing "money in reserves" constitutes a capital reserve study. In reality, it does not. The study is the analysis, not the account balance.

Who must comply: condos, co-ops, and planned real estate developments

New Jersey's reserve study law reaches broadly. Condominium associations, cooperatives, and planned real estate developments are subject to New Jersey reserve study requirements when their common-area capital assets exceed $25,000. That threshold captures most communities in the state, both small and large.

The requirement traces back to legislation amending the Planned Real Estate Development Full Disclosure Act, known as PREDFDA. The mandate arrived through S2760, which established the reserve funding requirements and the five-year update cycle. It was later refined by S3992. New Jersey is not alone here; the broader landscape of New Jersey's Structural Integrity and Reserve Study law (P.L. 2022, c.50) tied structural inspections to reserve funding for the first time. If your community was created under PREDFDA and manages common elements, consult your association attorney to determine whether you are covered. You can read the enacted text of S2760 on the New Jersey Legislature site to confirm the statutory language.

What actually happens here trips up many boards. They assume that "planned real estate development" refers only to large master-planned communities. It does not. A 24-unit condo building with a shared boiler and parking lot qualifies just as much as a 400-home planned real estate development. The confusion comes from the name, which sounds bigger than the legal definition. A New Jersey reserve study applies based on ownership structure and shared asset value, not community size. If you operate across state lines or want to compare mandates, our overview of reserve study requirements by state breaks down how the rules differ.

Exemptions from NJ reserve study requirements

Not every association has to file a full study, and knowing where reserve study exemptions apply can save smaller communities real money. The clearest exemption is the dollar threshold. If your common area capital assets do not exceed $25,000 in total repair and replacement value, the requirements generally do not apply to you. Think of a small homeowners association with only a single entrance sign and a strip of landscaping.

Communities without meaningful common elements can also fall outside the mandate. If homeowners individually own and maintain their roofs, exteriors, and grounds, and the association holds no significant capital assets, there may be little for reserve study exemptions to matter or a study to analyze.

Here is the hard truth, though: exemptions are narrower than boards want them to be. Most boards that assume they qualify actually do not. They underestimate the value of paving, drainage, or shared utility systems. One self-managed board in a small townhome cluster assumed their $25,000 exemption applied because their only obvious shared asset was landscaping; then a reserve inventory valued their private roads and storm drainage well past the threshold, leaving them behind on required contributions. Whether a New Jersey reserve study is required varies based on your governing documents and asset inventory, so confirm with your association attorney rather than guessing. Getting the exemption question wrong means discovering, years later, that you were out of compliance the whole time.

The reserve study process step-by-step (inspection, life cycle analysis, funding plan)

The reserve study process runs in a predictable sequence. First comes the site inspection. A Reserve Specialist, licensed engineer, or architect visits the property and documents every common-area capital asset by measuring, photographing, and assessing its condition. For newer communities, this may be tied to a transition study when the developer hands control to homeowners. That transition study establishes the baseline inventory.

Second is the life cycle analysis. Each component gets a remaining useful life and a replacement cost. A parking lot might have 12 years left; an elevator, 20. This is the physical analysis feeding directly into the numbers.

Third, the financial analysis builds the funding plan. The study models your reserve funds forward across a 30-year horizon. It then calculates the contributions needed to stay ahead of the repair schedule, protecting budget stability year over year. Integrated financial management tools can keep that funding plan tied to your operating budget so the two never drift apart. This is where the 85 percent funding option often enters the conversation. Many boards target the 85 percent funding option to demonstrate adequate reserves without overfunding to 100 percent, which keeps contributions manageable while still satisfying the statute.

Fourth, you receive the deliverable: a written report that includes the component inventory, funding recommendations, and compliance documentation. Then the cycle repeats, because a reserve study update is required at least every five years. The reserve study cost varies with size and complexity, but for most small to mid-size associations, a capital reserve study runs a few thousand dollars, far less than the reserve fund deficiencies it catches.

Why reserve studies matter for long-term community stability

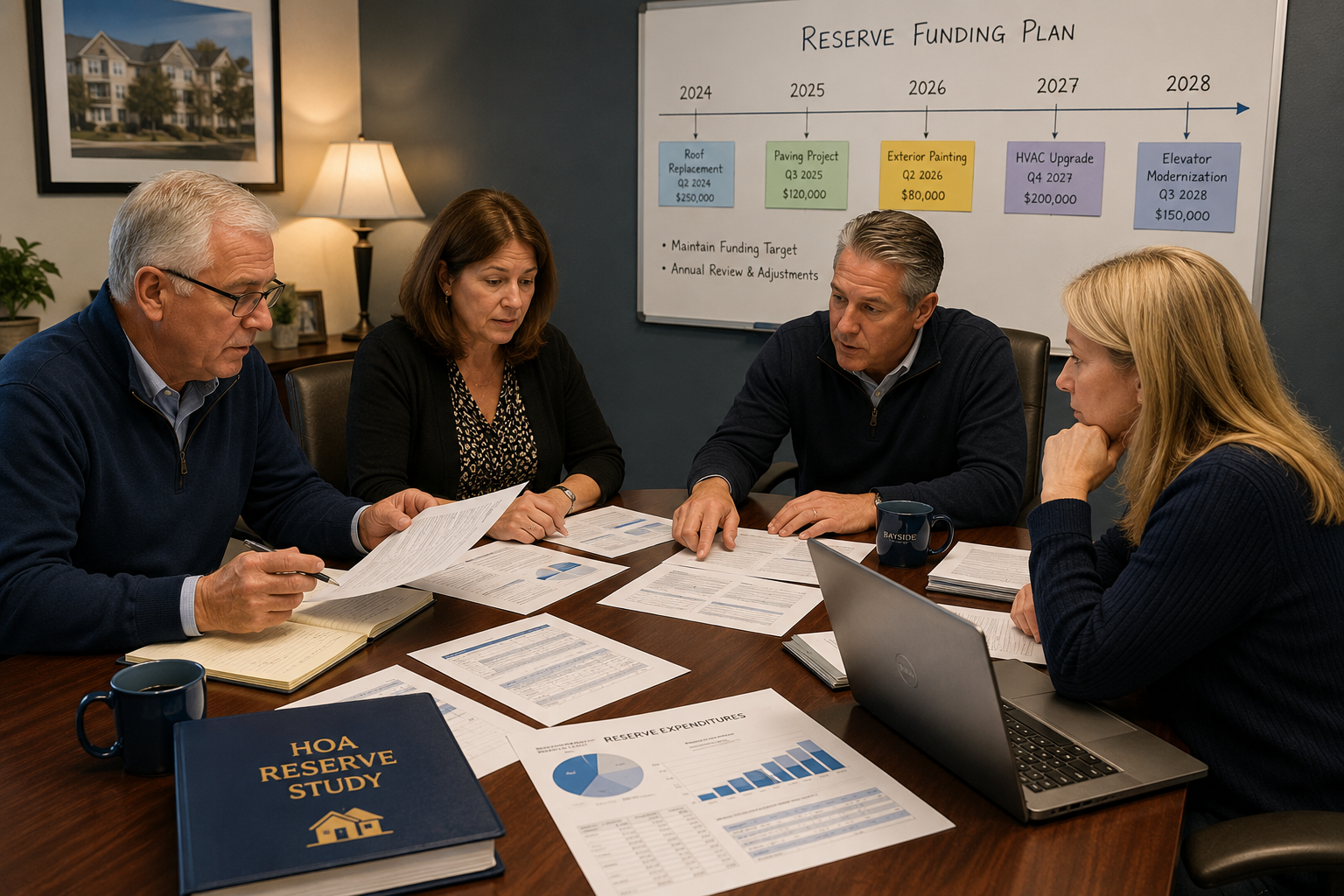

Reserve studies matter because deferred maintenance never gets cheaper. It compounds. A retaining wall that needs $8,000 in repairs this year becomes a $40,000 emergency after five more winters of freeze-thaw damage. The association that did not plan for it hits homeowners with a special assessment nobody saw coming. The mechanism is simple: small problems left unaddressed accelerate the failure of the components around them, so the longer a board waits, the wider the funding gap grows.

The 2021 Surfside condominium collapse in Florida killed 98 people. It put a brutal spotlight on what underfunded reserves and ignored structural warnings can produce. That tragedy drove much of the reserve study law reform across the country, including here. In the wake of Surfside, Florida's reserve study law became one of the strictest in the nation, and New Jersey followed with its own structural inspections and reserve funding requirements. These exist because the consequences of neglect eventually become physical ones.

Adequate reserves also protect property values. Buyers and their lenders increasingly scrutinize an association's reserve funds before closing, and a community with deficiencies can watch sales stall. Long-term planning through a New Jersey reserve study keeps dues predictable and budgets stable. Boards that fund reserves steadily avoid the boom-and-bust cycle. Homeowners plan their own finances around a dues number that does not lurch. That stability, in practice, is the visible result of financial responsibility done quietly over decades.

Practical compliance steps and board documentation for NJ boards

Start by locating your last reserve study, if one exists, and checking its date. If it is older than 5 years or you have never had one, you are likely out of compliance and should act quickly. Note your compliance deadlines. Condominium associations that had not studied since January 8, 2019, faced early compliance deadlines under S2760, which was later refined by S3992, the statute that amended PREDFDA. Newer associations have their own timelines tied to formation.

Next, engage a qualified provider: a credentialed Reserve Specialist, engineer, or architect. Do not hand this to a general handyman or a board member's spreadsheet. The reserve study law requires specific credentials; a non-qualified study will not satisfy the reserve study requirements. The reason the statute names those credentials is that a defensible funding plan depends on accurate remaining-life and cost estimates, which take training a general contractor does not have.

Then document everything. Keep the completed study, the funding plan, board meeting minutes approving reserve contributions, and evidence you have adopted the recommended funding levels. This documentation is your proof of financial responsibility if a homeowner or regulator questions your process. Board members share fiduciary board responsibility here, and organized records are the clearest defense of that responsibility.

Finally, build the reserve contribution into your annual budget and schedule your next reserve study update before the five-year mark. If you need a starting point, our step-by-step HOA budget guide walks through folding reserve contributions into your operating plan. Treating compliance as an ongoing rhythm, rather than a one-time scramble, separates boards that stay ahead from boards that get caught short.

Compliance tracking tools for self-managed and volunteer-run NJ boards

Self-managed communities carry the same reserve study requirements as professionally managed ones. Without a management company tracking deadlines, though, things slip. A volunteer treasurer with a full-time job forgets that the five-year clock is ticking. The board only realizes it is overdue when a lender flags it during a home sale. This is the gap that catches self-managed communities most often.

The fix is systematizing the tracking so it does not depend on any one person remembering. Platforms like Solume include automated tools that flag upcoming compliance deadlines and keep the funding plan tied to your budget for lasting budget stability. That matters most for volunteer-run boards without dedicated staff. For very small communities, mastering the bookkeeping basics for small HOAs first makes reserve tracking far easier to sustain.

The point is not the software for its own sake. It is that reserve funding requirements demand consistency over years, and human memory is a fragile place to store a five-year obligation. Board members turn over. Treasurers move away. What many communities don't realize is that most compliance failures aren't caused by boards deciding to skip the study. They are caused by nobody being assigned to watch the calendar. Whatever tool you use, whether a spreadsheet, a calendar reminder, or a dedicated platform, the goal is the same: make the deadlines impossible to miss even as your board changes.

Reserve study transparency and communicating funding status to homeowners

A completed reserve study only builds trust if homeowners actually see it. Financial transparency is where a lot of boards lose their community's confidence. Not because they are hiding anything, but because they never share the numbers. Owners assume the worst when they are kept in the dark.

Share the study's headline findings at your annual meeting: your percent-funded level, the annual contribution the plan recommends, and the major components coming due in the next few years. When homeowners understand that this year's dues increase funds a roof replacement scheduled for 2031, resistance softens. People accept costs they understand.

Be honest about reserve fund deficiencies if you have them. A board that says "we are at 55 percent funded and here is our five-year plan to reach adequate reserves" earns more trust than one that stays vague. When a board keeps funding status buried in a filing cabinet, homeowners default to suspicion at exactly the moment a special assessment lands; Solume gives boards financial reporting and a centralized communication hub so reserve planning stays visible to residents year-round.

Transparency also protects the board. When homeowners have seen the reserve study process and the funding plan year after year, a special assessment, if one ever becomes necessary, arrives as an understood contingency rather than a betrayal. This financial transparency is where board responsibility and long-term planning meet: fewer disputes, more buy-in, and steadier community stability.

If your board wants a clearer way to manage reserve planning, compliance tracking, and homeowner communication without leaning on a management company, you can see how it works for self-managed communities with Solume in a quick 15-minute call. It is worth finding out whether the reserve study tools and transparency features fit your community before your next compliance deadline arrives.

Frequently Asked Questions

What exactly is a reserve study for a New Jersey HOA?

A reserve study is a professional assessment of your community's shared capital components: like roofs, roads, and elevators: that estimates their remaining life and future repair or replacement costs. It includes a 30-year funding plan designed to cover those costs without relying on special assessments or loans.

How often does my New Jersey community need to update its reserve study?

State law requires the reserve study to be updated at least every five years. Many boards choose to revisit their numbers more frequently because construction costs and component conditions can shift significantly between updates.

Is a reserve study really worth the cost for a small self-managed HOA?

For most boards, the study costs far less than a single unplanned special assessment or emergency loan caused by underfunding. Beyond the financial protection, it's now a legal compliance requirement in New Jersey, so skipping it exposes the board to liability.

What happens if our board ignores the reserve study requirement?

Non-compliance leaves the board vulnerable to legal exposure, homeowner disputes, and the financial fallout of deferred maintenance that eventually forces large special assessments. Underfunded reserves can also lower property values and make it harder for owners to secure financing.

Our community was formed before 2019: do we still need to comply?

Yes. Associations that had not conducted a reserve study since January 8, 2019 were required to complete one under the initial deadlines, and newer associations formed after January 2025 must undertake their own study. All qualifying communities remain on the five-year update cycle going forward.