Most Maryland boards don't realize they're already out of compliance. The reserve study law passed years ago, but enforcement and awareness lagged. Now, with HB 292 adding reserve funding requirements effective October 1, 2025, the risk of noncompliance has become real. If your community hasn't completed a mandatory reserve study in the last five years, you're operating without the financial roadmap that Maryland HOA reserve study requirements in Maryland demand.

Key Takeaways

- Maryland HOA reserve study requirements in Maryland mandate that condominium associations, homeowners associations, and cooperative housing corporations complete a reserve study at least every five years under House Bill 107

- HB 292 adds reserve funding requirements starting October 1, 2025, requiring the board of directors to follow a funding plan based on their reserve study or document why they're deviating

- Communities with annual budgets under the $10,000 threshold are exempt from reserve study requirements, but most Maryland communities exceed this amount

- Reserve studies must include an on-site inspection, inventory of common components, estimated useful life and replacement costs, and a recommended funding plan

- The board of directors must review their reserve study annually during budget preparation and provide a reserve study summary to all lot owners or unit owners

- Non-compliance exposes boards to personal liability, special assessments, and potential legal action from homeowners

- Maryland boards that wait until 2026 to start their reserve study will miss the compliance window and face immediate funding pressure

Overview of Maryland HOA Reserve Study Requirements Under House Bill 107

House Bill 107 established Maryland's reserve study framework. The law applies to communities governed by the Maryland Condominium Act, the Maryland Homeowners Association Act, and cooperative housing corporations.

Here's what the law requires: every covered community must obtain an independent reserve study at least once every five years. The study must evaluate all major common components, estimate their remaining useful life, project replacement costs, and recommend a funding plan to avoid special assessments.

The law doesn't just ask for a reserve study. It defines what qualifies. The study must be prepared by a qualified reserve specialist or firm with experience in reserve analysis. A board member with a spreadsheet doesn't meet the standard. Neither does a property manager's rough estimate.

Maryland reserve study law also requires boards to review the study annually and incorporate its findings into the annual budget process. This isn't a one-time exercise. It's an ongoing long-term capital planning obligation.

Most Maryland communities assume they're compliant because they completed a study years ago. If that study is more than five years old, you're out of compliance. The five-year reserve study clock resets with each update. The reason this matters: Maryland HOA reserve study requirements tie directly to the board's fiduciary duty, and outdated studies provide no legal protection when component failures trigger special assessments.

Which Maryland Community Types Must Comply With Reserve Study Requirements

Three community types fall under Maryland HOA reserve study requirements:

Condominium associations governed by the Maryland Condominium Act must comply. This includes high-rise condos, townhome condos, and mixed-use developments with residential units.

Homeowners associations governed by the Maryland Homeowners Association Act must comply. This covers planned communities in Prince George's County, Montgomery County, and throughout Maryland, including single-family HOAs and townhome communities structured as HOAs rather than condos.

Cooperative housing corporations must comply. Co-ops are less common in Maryland but face the same reserve study requirements as condos and HOAs.

The $10,000 threshold provides the only exemption. If your community's annual budget falls below this amount, you're exempt from the requirement. In reality, almost no functioning community operates on less than this. Insurance alone typically exceeds that amount.

A developer-controlled board has a grace period. Communities still under developer control aren't required to complete a reserve study until control transitions to homeowners. Once the transition happens, the five-year clock starts.

Single-family home communities without common elements sometimes assume they're exempt. If you have shared roads, a clubhouse, a pool, or any other common components requiring future replacement, you're subject to reserve study requirements regardless of home type.

Five-Year Reserve Study Frequency and Update Requirements in Maryland

Maryland reserve study law requires a full update every five years. This isn't optional. The statute specifies that the study must be updated "at least once every five years."

What counts as an update? A full reserve study includes a new on-site inspection, updated component inventory, revised useful life estimates, current replacement cost projections, and a recalculated funding plan.

Some boards try to stretch the timeline by calling an internal spreadsheet review an "update." That doesn't satisfy the legal requirement. The update must be prepared by a qualified reserve specialist using current data.

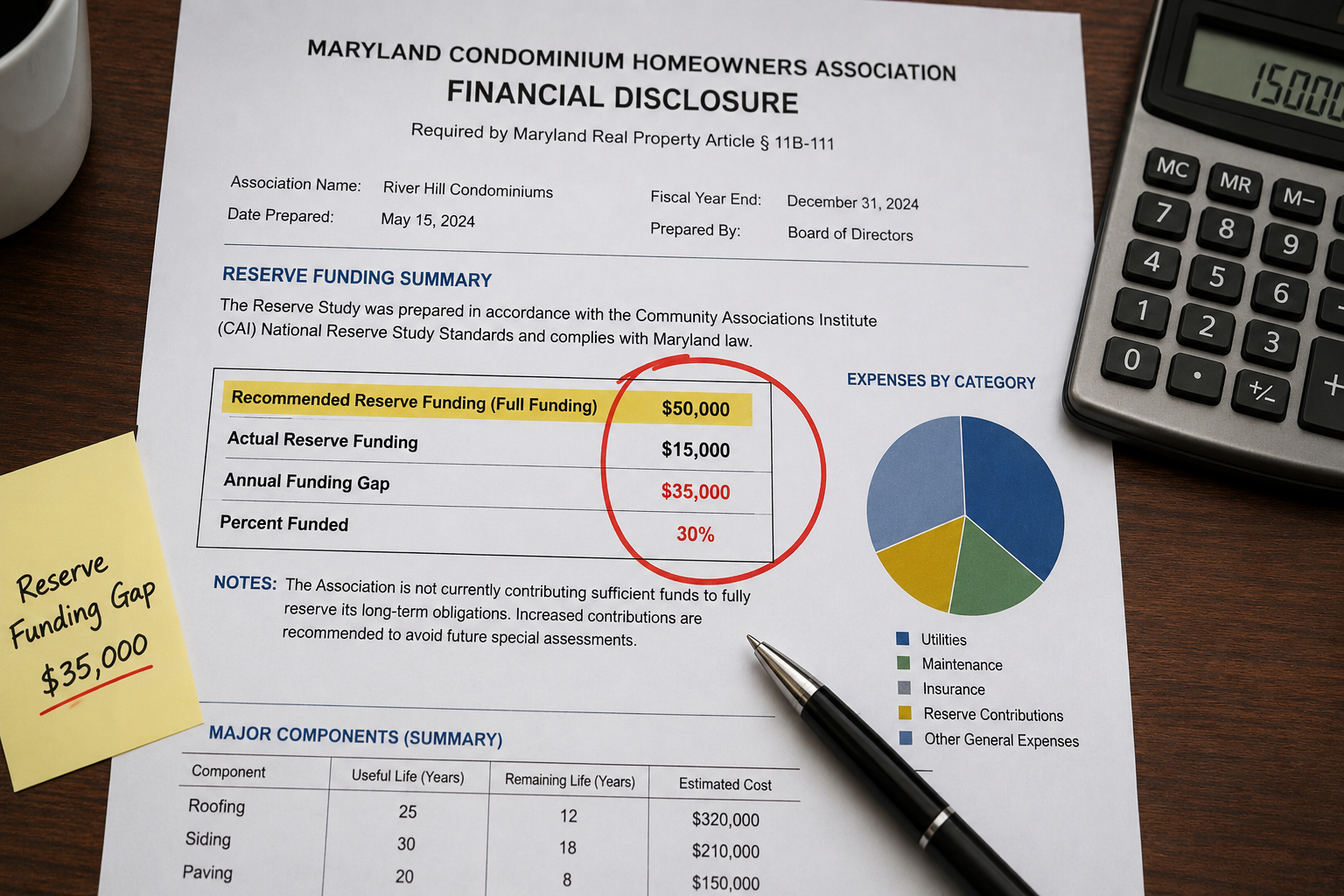

Between full updates, boards should conduct annual reviews. The annual budget process requires boards to compare actual reserve contributions against the reserve study's recommended funding plan. If you're underfunding, you need to document why and explain the risk to homeowners.

Reserve study frequency matters because replacement costs change. A roof that cost $150,000 to replace in 2020 might cost $200,000 in 2025. Inflation, material costs, and labor rates all shift. A five-year-old study with outdated cost projections creates a false sense of security.

The risk most boards overlook: if your last study was completed in 2019, it expired in 2024. You're already out of compliance. Starting the process now means you won't have a completed study until mid-2025 at the earliest.

New Mandatory Funding Requirements Under HB 292 Effective October 1, 2025

HB 292 changes everything. Before this law, Maryland required reserve studies but didn't mandate that boards actually fund them. Boards could complete a study, see that they needed to contribute $50,000 annually, and then contribute $10,000 instead. Homeowners had no recourse.

Starting October 1, 2025, that loophole closes. HB 292 establishes reserve funding requirements that boards must adopt and follow based on their reserve study. If the study recommends $50,000 in annual contributions, the board must either fund that amount or formally document its reasons for deviating.

The law includes a financial hardship exception. If full funding would impose unreasonable financial hardship on homeowners, the board may adopt an alternative plan. But here's the catch: the board must document the hardship, explain the alternative plan, and disclose the risks of underfunding to all unit owners or lot owners.

This shifts liability. Before HB 292, boards could quietly underfund reserves and hope for the best. Now, if a board underfunds and then hits homeowners with a $500,000 special assessment, those homeowners have a clear legal argument: the board violated its mandatory funding obligation.

HB 292 also requires annual disclosure. Every year, the board must provide homeowners with a summary showing actual reserve contributions versus the recommended funding plan. If there's a gap, homeowners see it in writing.

Most Maryland boards haven't adjusted their 2026 budgets to reflect the October 1, 2025, effective date. They're still budgeting based on what homeowners will tolerate rather than what the reserve study requires. That approach becomes legally indefensible after October 1, 2025.

Annual Budget Preparation and Reserve Study Review Obligations

Maryland law requires boards to review their reserve study annually during budget preparation. This isn't a suggestion. It's a compliance requirement tied to the budget approval process.

Here's what the annual review must include: compare the current reserve fund balance to the reserve study's projected balance, evaluate whether actual contributions align with the funding plan, assess whether any components have deteriorated faster than projected, and determine whether cost estimates require adjustment.

The annual budget must reflect reserve study findings. If your study recommends $40,000 in annual contributions but your budget only allocates $15,000, you're creating a documented compliance gap.

Boards must also provide disclosure to homeowners. Maryland law requires that lot owners and unit owners receive a reserve study summary along with the annual budget. The summary must show the current reserve balance, the recommended funding level, the actual funding level, and any known shortfalls.

Many Maryland boards skip this disclosure requirement entirely. They approve the budget, send out assessment notices, and never mention the reserve study. That's a violation of disclosure requirements under both House Bill 107 and HB 292.

The annual review also protects boards from liability. If you review the study annually, adjust for changing conditions, and document your funding decisions, you demonstrate a fiduciary duty. If you ignore the study for five years and then face a crisis, you've failed that duty. Why this matters: Maryland courts hold board members personally liable for breaches of fiduciary duty, and ignoring statutory reserve requirements provides clear evidence of that breach.

Practical Action Plan and Compliance Timeline for Maryland Boards

If your board hasn't completed a reserve study in the last five years, start now. Here's the timeline:

Month 1: Obtain proposals from at least three qualified reserve specialists. Verify that each firm has experience with Maryland communities and understands compliance requirements. Check references from other Maryland boards.

Month 2: Select a provider and schedule the on-site inspection. The specialist will walk the property, photograph components, and document current conditions. Board members should participate in the walkthrough to understand what's being evaluated.

Month 3: Receive the draft reserve study. Review the component inventory, useful life estimates, and replacement cost projections. Challenge any assumptions that seem off. A good reserve specialist will explain their methodology.

Month 4: Finalize the study and present it to the full board. Schedule a special meeting if necessary. Every board member should read the executive summary at a minimum.

Month 5: Incorporate the reserve study into your next annual budget. Calculate the recommended contribution level and compare it to your current funding. If there's a gap, decide whether to close it immediately or phase in increases over multiple years.

Month 6: Provide the reserve study summary to all homeowners along with the proposed budget. Explain what the study found, what it recommends, and what the board is proposing to do about it.

For boards that already have a reserve study, the action plan is simpler: review it annually, fund it in accordance with HB 292 requirements, and schedule your next update before the five-year deadline.

The compliance timeline for HB 292 is tight. If you're starting from zero in 2025, you need to complete the study, adjust your funding plan, and implement the mandatory funding plan by October 1, 2025. That's why boards waiting until 2026 will already be out of compliance.

Here's a scenario that plays out every year: a 75-unit Montgomery County condo completes its reserve study in March, discovers it's 40% funded when it should be at 70%, and faces a choice. The board can phase in a $200-per-month assessment increase over three years, or hit owners with a $150,000 special assessment when the roof fails in 18 months. Boards that choose gradual increases survive. Boards that ignore the gap face owner lawsuits and board recalls when the emergency hits.

Common Mistakes Maryland Boards Make With Reserve Studies and How to Avoid Them

Mistake 1: Treating the reserve study as a one-time project. Boards complete the study, file it away, and never look at it again. The study is only useful if you review it annually and adjust your funding accordingly.

Mistake 2: Choosing the cheapest provider. Reserve studies range from $2,000 to $8,000 depending on community size and complexity. The cheapest bid usually means the least thorough analysis. A bad study is worse than no study because it creates false confidence.

Mistake 3: Skipping the on-site inspection. Some boards try to save money by providing photos and documents instead of paying for an on-site visit. Maryland reserve study law requires an on-site inspection. Remote studies don't meet the legal standard.

Mistake 4: Ignoring the funding recommendation. The study says you need $60,000 per year, but the board only budgets $20,000 because that's what homeowners will accept. Under HB 292, that's a compliance violation unless you document the financial hardship exception.

Mistake 5: Failing to disclose the study to homeowners. Disclosure requirements exist for a reason. Homeowners have a right to know the community's financial condition. Boards that hide reserve shortfalls face legal exposure when the special assessment arrives.

Mistake 6: Using an unqualified preparer. Your property manager's intern with an Excel spreadsheet is not a qualified reserve specialist. Neither is a board member with a background in finance. The study must be prepared by an independent professional with experience in reserve studies.

Mistake 7: Waiting until components fail. Some boards delay the reserve study until the roof starts leaking or the parking lot cracks. By then, you're in crisis mode. The whole point of reserve planning is to avoid emergencies from deferred maintenance and the costly special assessments that follow years of neglect. According to the Appraisal Institute's guidance on property valuation, accurate cost projections are essential for effective reserve planning.

Mistake 8: Assuming small communities are exempt. Unless your annual budget is under $10,000, you're not exempt. Community size doesn't matter. A 20-unit condo has the same reserve study requirements as a 200-unit community.

Many boards assume that if homeowners don't complain about assessments, the reserve funding must be adequate. In reality, homeowners don't understand reserve adequacy until a major component fails and they receive a $10,000 special assessment notice. By then, the board has already failed its fiduciary duty.

How Reserve Study Automation and Software Tools Help Maryland Boards Stay Compliant

Manual reserve tracking creates compliance risk. Boards that manage reserves in spreadsheets or paper files struggle to maintain the annual review cycle required under Maryland reserve study law. When your reserve study sits in a PDF buried in someone's email from 2021, you can't track whether you're meeting HB 292 funding requirements or approaching your five-year update deadline.

Reserve study automation solves several problems at once. First, it centralizes the reserve study data so every board member can access current projections. Second, it tracks actual contributions against the recommended funding plan, making HB 292 compliance reporting automatic. Third, it alerts boards when the five-year update deadline approaches.

Solume's reserve study integration connects your reserve study directly to your annual budget and financial reporting. When you prepare the annual budget, the system shows your current reserve fund balance, your funded percentage, and the contribution level needed to stay on track. You don't have to dig through a PDF or remember where you filed the study three years ago.

The system also generates the reserve study summary required for homeowner disclosure. Instead of manually creating a summary document each year, the platform produces a compliant disclosure report that compares actual versus recommended funding.

For Maryland boards managing compliance across multiple requirements, automation reduces the administrative burden. You're not just tracking reserves. You're also managing vendor contracts, maintenance requests, governing documents, and homeowner communications. Integrated software keeps everything in one place.

Boards that use reserve study automation also avoid the common mistake of forgetting to review the study annually. The system prompts you during budget season to compare your funding plan against the reserve study recommendations.

The transparency benefit matters too. When homeowners can log in and see the reserve study summary, the current funded percentage, and the projected replacement schedule, trust increases. Boards that hide reserve information create suspicion. Boards that share it demonstrate financial responsibility.

Maryland HOA reserve study requirements in Maryland aren't going away, and HB 292 makes compliance mandatory starting October 1, 2025. Boards that act now have time to complete their studies, adjust their funding plans, and phase in any necessary increases in assessments. Boards that wait face compressed timelines, homeowner backlash, and potential liability.

Ready to simplify reserve study compliance for your Maryland community? Explore your options with Solume's team to see how integrated reserve planning, automated compliance tracking, and transparent homeowner reporting can protect your board and your community's financial future.

Frequently Asked Questions

Does Maryland law actually require HOAs to do reserve studies?

Yes. House Bill 107 requires condominium associations, homeowners associations, and cooperative housing corporations to complete a reserve study at least every five years unless their annual budget is under the $10,000 threshold.

What exactly needs to be included in a Maryland HOA reserve study?

The study must include an on-site inspection, a complete inventory of common components, estimated useful life for each component, current replacement cost projections, and a recommended funding plan to avoid special assessments.

How often do Maryland HOAs need to update their reserve studies?

Maryland reserve study law requires a full update at least once every five years. Boards must also review the study annually during budget preparation and adjust funding as needed.

Can a Maryland HOA board skip the reserve study if homeowners vote against it?

No. Reserve study requirements are statutory, not optional, and homeowner votes cannot override Maryland reserve study law.

What happens if our Maryland HOA hasn't done a reserve study in over five years?

You're currently out of compliance with Maryland HOA reserve study requirements. Start the process immediately to minimize liability exposure, and be prepared to explain the delay if homeowners or regulators ask.

How much should a Maryland HOA actually be setting aside in reserves each year?

The reserve study calculates the specific amount based on your common components, their condition, and replacement timelines. Under HB 292, boards must follow the funding plan or formally document any deviations, and the Community Associations Institute provides resources to help boards understand appropriate funding levels.

Is the reserve study requirement worth the cost for a small Maryland community?

Yes. Even small communities face major expenses like roof replacement, siding repair, or road resurfacing, and the cost of a reserve study ($2,000 to $5,000) is far less than the cost of an emergency special assessment.

What's the difference between HB 107 and HB 292 for Maryland reserve studies?

HB 107 requires boards to complete reserve studies every five years, while HB 292 requires boards to actually fund those studies according to reserve funding requirements starting October 1, 2025.