KEY TAKEAWAYS

- A reserve study contains two separate analyses: a physical inspection of your community's common area components and a financial funding model that projects how much money you need to collect to replace them. Both halves can fail independently.

- Physical analysis assesses the real, current condition of tangible assets — roofs, elevators, pavement, HVAC systems, pools — and estimates their remaining useful life. This is your data foundation. If it is inaccurate, everything built on top of it is inaccurate.

- Financial analysis translates that physical data into a long-range funding plan. It accounts for inflation, interest earned on reserve balances, expenditure timing, and your community's current funded status relative to its projected obligations.

- A community can have a healthy-looking reserve balance and still be financially underprepared — if the physical inspection underlying the model is outdated or the cost projections are too optimistic.

- Reserve funding adequacy is now a mortgage eligibility issue in the United States. Fannie Mae and Freddie Mac have updated condo project requirements to include reserve funding standards. Underfunded communities can affect homeowners' ability to sell or refinance.

- Consistent, adequate reserve funding is the HOA equivalent of financial hedging — it eliminates the uncertainty around future replacement costs before those costs arrive.

- Solume transforms your static reserve study PDF into a dynamic financial model your board can actively manage. And through our national network of reserve study partners, we can connect you with the right professionals for your physical inspection.

Most HOA and condo boards think of a reserve study as a single document. It arrives as a PDF, sits in a shared drive, gets referenced during budget season, and collects digital dust the rest of the year.

That is the first mistake.

A reserve study is actually two separate analyses bundled into one report. There is the physical analysis — a professional inspection of every major common area component your community owns. And there is the financial analysis — a long-range funding model that projects how much money you need to collect, and when, to cover the replacement costs those components will eventually generate.

Both halves matter. Both halves can fail independently. And most boards, when they review a reserve study, are only paying attention to one of them.

Understanding the distinction between physical vs financial analysis is not just an academic exercise. It is the difference between a community that is genuinely financially prepared and one that is flying blind with a false sense of security. This guide breaks down both sides, explains what can go wrong with each, and shows how HOA and condo boards can use this framework to make smarter decisions in 2026 and beyond.

Understanding Physical Analysis in Markets

Exploring Physical Assets and Tangible Markets

Physical analysis, at its most fundamental level, is the assessment of tangible assets — things you can see, touch, inspect, and measure. In the broader world of financial markets, physical analysis applies to real estate, crude oil, precious metals, and other commodities that exist in the physical world. These are assets with intrinsic value derived from their physical properties, their condition, and their remaining useful life.

In a commodity context, the physical market refers to transactions involving actual physical delivery of a commodity — a buyer and seller exchanging a real thing, not just a contract. The spot market is where those transactions happen in real time, based on current supply and demand conditions. Price in the physical market reflects the tangible reality of what an asset is, where it is, and what condition it is in.

For HOA and condo communities, physical analysis means exactly the same thing. Your community owns tangible assets — roofs, parking lots, elevators, HVAC systems, pool decks, fencing, irrigation systems, retaining walls, and common area lighting. These assets have physical properties that determine how long they last and what they cost to replace. Physical analysis is the process of inspecting those assets, measuring their condition against expected lifespans, and projecting when each component will need to be repaired or replaced.

This is not a financial exercise. It requires a trained professional walking your property, not a spreadsheet model. The physical inspection is your spot market — it tells you the real condition of your real assets, right now, without financial assumptions layered on top.

Case Studies: Real-World Applications

Consider a mid-rise condominium in Atlanta with 120 units. The building has three elevators installed in 2008 with an expected useful life of 25 years. A proper physical analysis does not simply note "elevators, installed 2008." It examines the current mechanical condition, identifies whether maintenance history has extended or shortened expected life, assesses recent service records for early warning signs, and projects a realistic replacement window — in this case, likely 2030 to 2033 depending on current condition and usage patterns.

That physical information is what drives the financial model. Get it wrong and everything downstream is wrong.

Now consider a homeowners association managing a large community with extensive common area infrastructure, including roads, a clubhouse, two pools, and landscaping hardscape. Physical analysis of asphalt paving requires measuring pavement condition index scores, crack density, and drainage performance — not simply noting the year of installation. A road that has been sealed and maintained regularly has a meaningfully different remaining life than one that has been deferred. The physical market conditions of the asset — its real, current condition — must inform the financial projections.

In the energy market, traders managing physical commodities like natural gas understand that supply risk is real and immediate. A pipeline outage or storage disruption has immediate price consequences. HOA boards managing physical infrastructure face the same supply risk dynamic: when a roof fails before its projected replacement date, the board cannot wait for a futures market to hedge the exposure. The cash has to be there. That is why physical analysis must be accurate — not conservative, not optimistic, but accurate.

Financial Analysis: Key Concepts and Applications

Diving into Financial Instruments and Contracts

If physical analysis answers "what do we have and what condition is it in," financial analysis answers "how do we pay for what comes next."

In global financial markets, participants use a range of financial instruments to manage future obligations and price risk. Futures contracts allow buyers and sellers to lock in a fixed price for a commodity at a future date, providing certainty in an uncertain market. Financial contracts of various structures — swaps, options, forward agreements — give market participants tools to match their known future cash flows against projected costs. The futures market exists precisely because the gap between today and tomorrow carries real financial risk.

HOA and condo reserve finance is built on the same logic, even if the terminology sounds different.

A reserve funding plan is, in effect, a long-range financial model that projects future cash flows — the monthly dues collected into reserves — against projected future expenditures on component replacements. The reserve study's financial analysis section must account for inflation (the equivalent of price risk in commodity markets), interest earned on invested reserve funds (the equivalent of yield on financial instruments), the timing and sequencing of expenditures, and the current funded status of the reserve account relative to the ideal.

The key financial instruments in HOA reserve management are the percent funded metric and the threshold funded model. Percent funded measures how much of the theoretical maximum reserve liability is actually funded. Threshold funding sets a floor — typically 10 to 30 percent — below which the board commits not to let reserves fall. Both are financial analysis tools, not physical ones. They say nothing about the condition of your roof. They say everything about whether your community has the financial capacity to deal with that roof when the time comes.

Interest rates matter here in a direct way. The assumed rate of return on invested reserve funds affects the funding requirement meaningfully. A community earning two percent on its reserves needs to collect more each year than one earning four percent, assuming identical physical replacement schedules. Market volatility in short-duration fixed income markets — money market funds, CDs, short-term treasuries — affects the actual return HOAs and condo associations earn on their reserve balances. These are real financial market exposures, not abstractions.

Best Practices for Financial Hedging

The concept of financial hedging translates directly into HOA reserve strategy, even if boards do not use that language.

Hedging, in the financial markets context, means using financial instruments to offset price risk on an underlying asset. An energy company that knows it will need to purchase natural gas next winter buys futures contracts to lock in a price today, protecting against price increases between now and then. The hedge does not eliminate the cost — it eliminates the uncertainty around the cost.

HOA and condo boards hedge their future replacement costs through consistent, adequate reserve funding. A community that fully funds its reserves is, in effect, hedging against the price risk and timing risk of future component replacements. It has locked in its ability to pay, regardless of what happens to construction costs, labor markets, or material prices between now and the replacement date.

The risk management tools available to HOA financial managers include scenario-based reserve funding models, inflation-adjusted cost projections, and investment laddering strategies that match the maturity of invested reserve funds to projected expenditure timelines. Basis risk — the gap between a financial hedge and the actual underlying exposure — exists here too. A community that projects a roof replacement at $180,000 based on 2020 cost data and three percent annual inflation may discover in 2027 that roofing costs have risen faster than general inflation. The hedge was imperfect. The financial analysis did not fully reflect the physical market conditions.

Best practices for HOA financial reserve analysis include updating reserve studies on a full physical inspection cycle — typically every three to five years — with annual updates to cost assumptions in between. Diversified portfolio strategies for invested reserves help manage interest rate exposure without taking on inappropriate credit risk. And understanding price trends in construction, roofing, mechanical systems, and paving is as important for an HOA financial manager as monitoring commodity prices is for a trading house.

Comparing Physical vs Financial Analysis

This is where many HOA boards get into trouble: treating the physical and financial halves of a reserve study as if they were the same thing, or assuming that a passing grade on one means a passing grade on both.

Physical assets are tangible. Financial assets — or in this case, financial projections and reserve fund balances — are intangible. A community can have physically excellent assets and be financially underfunded for their replacement. It can also have a reserve account that looks healthy on paper but is built on a physical inspection that underestimated replacement costs or overestimated remaining useful life.

When you trade physical assets in the commodities world, you are dealing with real things subject to physical market conditions — wear, weather, supply disruptions. When you trade paper in financial markets, you are dealing with instruments whose value depends on models, assumptions, and market sentiment. The physical side relies on physical delivery; the financial side uses contracts and projections.

The same distinction holds in HOA reserve management. The physical side of your reserve study relies on physical delivery — meaning, your property is actually in the condition the inspector documented, and the replacement costs are grounded in current market prices for materials and labor. The financial side uses contracts and projections — meaning, your funding plan rests on assumptions about inflation, interest rates, future dues levels, and expenditure timing that may or may not prove accurate.

Price movements in construction and materials markets differ based on market conditions and sentiment, just as commodity prices do. Roofing material prices spiked dramatically during supply chain disruptions in 2021 and 2022. Concrete and masonry costs are sensitive to energy prices, since cement production is highly energy-intensive. An HOA board that ignores these commodity market dynamics in its financial analysis is making assumptions that may not hold.

Are financial assets more dependent on intellectual property and analytical methodology than physical ones? In the reserve study context, yes. The value of a high-quality reserve study financial analysis lies entirely in the rigor of the methodology — the depreciation models used, the inflation assumptions applied, the funding strategies recommended. That intellectual property is what separates a rigorous reserve study from a document that merely gives the appearance of financial planning.

The Role of Analysis in the United States and the United Kingdom

Regional Impacts on Commodities and Financial Markets

Reserve study requirements and practices vary significantly by region across the United States — and increasingly, reserve funding standards are becoming a regulatory and lending issue, not just a best practice.

In the United States, the post-Surfside regulatory environment has fundamentally changed the conversation. Florida's new structural inspection and reserve funding requirements — phased in starting in 2025 — represent the most significant shift in community association law in decades. Similar legislation is moving through multiple state legislatures. Fannie Mae and Freddie Mac have updated their condominium project eligibility requirements to include reserve funding adequacy as a condition of mortgage approval. Communities with inadequate reserves are finding that homeowners cannot sell — or cannot sell at full market value — because lenders will not write conforming mortgages on units in financially distressed associations.

Natural gas prices, oil price trends, and energy trading dynamics affect HOA and condo operating costs in direct ways that most boards underestimate. Energy commodities represent a significant portion of common area operating costs — pool heating, lighting, HVAC for common areas, and elevator power consumption. In markets with volatile natural gas prices or utility rate structures tied to commodity prices, HOA operating budgets face real commodity market exposure. Policy makers at both the state and federal levels, along with hedge funds and investment banks that influence bond and utility markets, shape the cost environment in which associations operate.

In the United Kingdom, leasehold reform and the shift toward commonhold ownership structures have placed new emphasis on reserve fund adequacy — called a "sinking fund" in the UK context. The challenges are structurally similar to those in the United States: physical assets that require long-range financial planning, communities with historically underfunded reserves, and growing regulatory pressure to correct the shortfall. Market volatility in construction costs following Brexit compounded the problem, as materials prices and labor costs shifted in ways that invalidated older reserve fund projections.

Climate Change and Market Adaptations

Climate change is reshaping the physical analysis side of reserve studies in ways that boards need to understand.

Energy systems in common areas are a direct example. Communities with aging HVAC systems are facing replacement decisions in a market where energy efficiency standards are tightening, refrigerant regulations are changing, and the cost differential between high-efficiency and standard equipment has narrowed considerably. The electricity market is in transition, and the equipment decisions HOA boards make today will lock in energy cost structures for the next 15 to 20 years. Physical analysis of common area energy systems needs to account for this transition, not just the age and condition of existing equipment.

Climate change is also accelerating wear on specific asset classes. Coastal communities face salt air corrosion, flooding risk, and wind damage profiles that have worsened. Southern communities face extreme heat that shortens pavement and roofing lifespan. Northern communities deal with freeze-thaw cycles that stress masonry, concrete, and waterproofing systems. An accurate physical analysis in 2026 must incorporate climate-adjusted lifespan assumptions — not the industry standard tables published 20 years ago.

For energy commodities consumed by associations, the transition toward renewable energy systems creates both opportunity and cost structure complexity. Solar installations on common areas, EV charging infrastructure, and LED lighting upgrades all involve capital expenditure that belongs in the reserve study if the useful life exceeds one year. Getting those assets into the physical analysis and properly funded in the financial model is an area where many communities are currently behind.

Long-term cost structure planning for the electricity market is increasingly relevant for high-rise communities with significant common area energy consumption. Utility rate structures are shifting in many markets, and communities that model future energy costs using historical averages may be systematically underestimating what they will actually pay.

Applications for Homeowners' Associations (HOAs)

How HOAs Benefit from Market Analysis

The most direct application of physical vs financial analysis thinking for HOA and condo boards is this: treat your reserve study as a two-part financial instrument, not a single document.

The physical inspection is your market data. It tells you what you own, what condition it is in, and what it will cost to replace. This data must be current, accurate, and conducted by qualified professionals. Stale physical data produces a misleading financial model regardless of how sophisticated the funding analysis is.

The financial funding model is your investment strategy. It tells you how to allocate current revenue — monthly dues collected into reserves — against projected future obligations. Optimizing that strategy requires understanding interest rates on invested balances, inflation trajectories for your specific asset classes, and the sequencing of expenditures across a 20 to 30-year projection window.

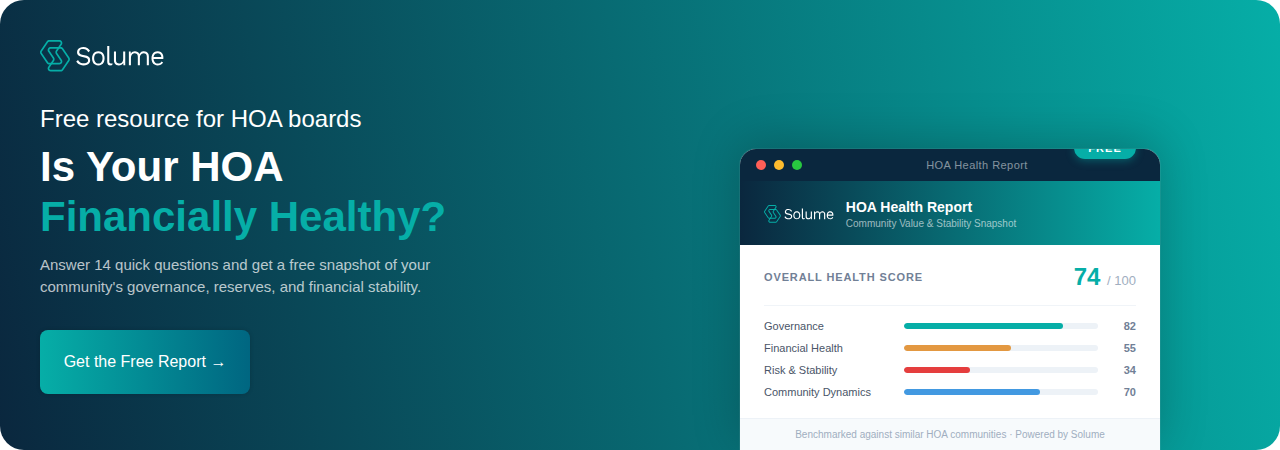

Taken together, these two elements define your community's financial position relative to its physical obligations. A community with a 70 percent funded reserve and a high-quality recent physical inspection is in a very different position than one with a 70 percent funded reserve built on a seven-year-old inspection with optimistic lifespan assumptions.

Revenue streams in HOA finance are largely fixed — assessments, late fees, transfer fees, and interest on reserves. Unlike a hedge fund or a commodity trading operation, associations cannot easily increase revenue when costs rise. This makes proactive financial analysis not just good practice but a structural necessity. Communities that underfund reserves are not just taking a financial risk; they are transferring that risk to future owners in the form of special assessments, deferred maintenance, and declining property values.

Using an AI-powered platform like Solume transforms this process meaningfully. Solume takes the static PDF output of your reserve study and converts it into a dynamic financial model — one that lets your board run funding scenarios, adjust inflation assumptions, model the impact of interest rate changes on your reserve balance, and see the projected funded status of your community at any point in the future. The reserve study becomes a living financial instrument, not a document that sits in a folder.

Solume does not provide reserve studies directly. But we partner with qualified reserve study providers across the United States who do. We can connect your community with the right professionals for your physical inspection — so that the data feeding your Solume financial model is accurate, current, and professionally certified.

Building Skill Sets for HOA Market Participants

Board members cycle in and out. Property managers handle multiple communities simultaneously. The institutional knowledge required to manage a reserve fund well is constantly at risk of walking out the door.

Building a genuine skill set around reserve analysis — understanding both the physical and financial components, knowing how to read a reserve study critically rather than just accepting its conclusions — is one of the highest-leverage things an HOA board can do.

On the physical side, this means understanding what a physical inspection actually involves, what credentials qualify a reserve study professional, and what questions to ask when reviewing the component inventory and useful life estimates. Are the lifespan assumptions conservative or optimistic? Are replacement costs based on current bid data or escalated from older figures? Is the component inventory complete, or are items missing that will create surprise expenditures?

On the financial side, understanding the difference between percent-funded and threshold-funded models, knowing how inflation assumptions affect long-range projections, and grasping how interest earned on reserve balances affects the required monthly contribution are all foundational concepts. These are not complicated — they are accessible to any board member willing to spend an hour with the material.

For deeper research, the Community Associations Institute publishes extensive guidance on reserve study standards and best practices. Academic literature indexed through Google Scholar and the Web of Science includes peer-reviewed research on the relationship between reserve funding adequacy and property values, the predictive validity of different reserve study methodologies, and the financial impact of deferred maintenance on community association balance sheets. Professionals seeking career progression in community association management increasingly find that reserve finance literacy is a differentiating skill set — one that clients and employers value specifically.

The value chain runs from physical inspection to component inventory to useful life and cost projection to funding analysis to annual budget recommendation to board vote. Understanding each link in that chain — and where errors can enter the process — is what separates boards that manage reserves well from those that discover the problem only when a special assessment becomes unavoidable.

Practical Takeaways for Market Participants in 2026

Reserve management is not getting simpler. Regulatory requirements are tightening, lender standards are rising, construction costs remain elevated, and the physical demands on community infrastructure are intensifying. Here is what HOA and condo boards should take into 2026:

Get a current physical inspection. If your last full reserve study is more than three years old, the physical data driving your financial model may no longer reflect reality. Component conditions change. Cost projections drift. A physical analysis grounded in current conditions is the non-negotiable foundation of everything else.

Treat your reserve fund as a financial instrument that requires active management. The funded status of your reserves is not a static number — it is a position that changes every month as contributions come in, interest accrues, and expenditures go out. Boards that check this number annually at budget time are managing reactively. Boards using platforms like Solume that make the model dynamic are managing proactively.

Adopt formal risk management strategies. In commodity trading, risk management tools exist to quantify exposure and protect against adverse outcomes. In HOA finance, the equivalent is maintaining adequate reserve funding levels, stress-testing your funding plan against inflation and cost overrun scenarios, and having a board policy that prevents raiding reserves for operating shortfalls.

Understand your price trends. Roofing, paving, mechanical systems, and pool equipment all have commodity prices that move with labor markets, materials costs, and energy costs. Boards that assume three percent annual inflation on all line items without examining actual price trends in their specific markets are making assumptions that may not hold. Work with your reserve study professional and your management company to ground your cost escalation assumptions in current market data.

Engage the right partners. Oil majors retain trading houses and investment banks for complex market exposure because they understand that specialized expertise pays for itself. HOA boards should work with qualified reserve study professionals for the physical analysis, CPAs experienced in community association finance for the financial planning, and purpose-built technology like Solume for the ongoing modeling and scenario analysis that keeps the board informed between reserve study cycles.

Do not let short-period market volatility — a spike in construction costs, an interest rate shift, an unexpectedly early component failure — become a crisis. The entire point of sound reserve management is to absorb those shocks without a special assessment. That buffer is only there if the board built it deliberately, over time, through consistent and disciplined reserve funding.

Reserve studies are not administrative paperwork. They are a physical and financial analysis of your community's long-term viability as a place where people want to own property.

The communities that treat them seriously — that invest in accurate physical inspections, maintain rigorous financial models, fund their reserves consistently, and use modern tools to keep their boards informed — are the communities that protect property values, avoid special assessments, and serve their homeowners well.

The communities that do not find out the hard way. Usually, when a roof fails, an elevator goes down, or a lender flags the community as ineligible for conforming mortgages, and a homeowner cannot close.

Solume exists to make sure your community never ends up in that second category.

Ready to see what a dynamic reserve study model looks like for your community?

Schedule a free 15-minute discovery call with our team — we will walk you through how Solume transforms your reserve study data into a living financial model your board can actually use.

Or sign up for a free 30-day trial and see the platform for yourself.

No commitment. No obligation. Just clarity on where your community stands — and what it takes to protect it.

FREQUENTLY ASKED QUESTIONS

What is the difference between physical and financial analysis in a reserve study?

A reserve study has two distinct components. The physical analysis is the on-site inspection conducted by a reserve study professional. It documents every major common area component your community owns, assesses its current condition, estimates remaining useful life, and projects the cost to repair or replace it. The financial analysis takes that physical data and builds a long-range funding model — projecting how much money the association needs to collect each month, at what assumed rate of return, to have the funds available when each replacement comes due. Physical analysis is about what you own and what condition it is in. Financial analysis is about whether you can afford to deal with it when the time comes.

Why does it matter if my reserve study is outdated?

Reserve studies have a physical inspection component that reflects conditions at a specific point in time. Component conditions change, replacement costs change, and climate and usage patterns affect useful life in ways that older studies cannot capture. Most reserve study professionals recommend a full physical inspection every three to five years, with annual financial updates in between. A community running a seven-year-old reserve study as the basis for its current funding model is making financial decisions on stale physical data, which means the financial projections may be meaningfully wrong even if the math is technically correct.

What does percent funded mean, and why does it matter?

Percent funded is a measure of how much of your theoretical maximum reserve liability is actually funded at a given point in time. If your community's components would cost $1,000,000 to replace all at once today, and your reserve account holds $600,000, you are 60 percent funded. A fully funded reserve — 100 percent — means you have exactly as much in reserves as the accumulated depreciation of your components would suggest you should. Most reserve study professionals consider 70 percent or above to be a healthy funded status, though the right target depends on your community's specific component mix and replacement schedule.

Can an underfunded reserve affect home sales in my community?

Yes, and this has become a more pressing issue in recent years. Fannie Mae and Freddie Mac — the two largest purchasers of conforming mortgages in the United States — updated their condominium project eligibility requirements to include reserve funding adequacy as a condition of approval. Lenders originating conforming loans must now review the association's reserve funding status as part of the approval process. Communities with inadequate reserves or deferred maintenance issues can be flagged as ineligible, which means buyers cannot obtain conventional financing on units in those communities. This directly affects market price and the ability of existing owners to sell or refinance.

What is a special assessment, and how does inadequate reserve funding cause one?

A special assessment is a one-time charge levied against all unit owners to cover a major expense the association's reserves cannot absorb. When a roof fails, an elevator requires emergency replacement, or a structural issue demands immediate repair, the board must find the money somewhere. If reserves are underfunded, the only options are a special assessment, an HOA loan, or deferred action — all of which are worse outcomes than having adequately funded reserves in the first place. Special assessments are disruptive, unpopular, and often inequitable because they charge current owners for the accumulated underfunding of previous years.

How does inflation affect HOA reserve fund projections?

Inflation affects reserve fund projections in two ways. First, it increases the projected replacement cost of every component over time. A roof that costs $150,000 to replace today will cost more in 10 years — how much more depends on inflation in roofing materials and labor, which does not always track general CPI. Second, it affects the purchasing power of the money sitting in your reserve account. A funding model that assumes three percent annual inflation but experiences five percent inflation in construction costs will consistently underproject replacement costs, leaving the community short when replacements come due. A good reserve study financial analysis uses asset-class-specific inflation assumptions rather than a single blanket rate.

What should HOA boards look for when reviewing a reserve study?

Boards reviewing a reserve study should examine both the physical and financial components critically. On the physical side: Is the component inventory complete? Are the useful life and remaining life estimates reasonable, given the actual condition documented in the inspection? Are replacement costs based on current market pricing or escalated from older data? On the financial side: What inflation rate is assumed, and is it appropriate for your specific asset classes? What interest rate is assumed on invested reserves, and is it realistic given current market conditions? What is the projected funded status of the reserve account over the next 10, 20, and 30 years under the recommended funding plan? And critically, what happens to that funded status if one or two major replacements come in over budget or ahead of schedule?

How does Solume help with reserve study management?

Solume takes the static PDF output of your reserve study and converts it into a dynamic financial model your board can actively work with. Rather than reviewing a reserve study once and filing it away, boards using Solume can run funding scenarios, adjust inflation and interest rate assumptions, model the financial impact of accelerating or deferring specific replacements, and track funded status in real time as contributions and expenditures flow through the account. Solume also integrates reserve fund data with the broader association financial picture — budgeting, dues collection, and operating expenses — so boards have a complete view of community financial health in one place. Solume does not provide reserve studies directly, but we partner with qualified reserve study providers across the United States and can connect your community with the right professionals for your physical inspection.

How often should an HOA or condo association update its reserve study?

The Community Associations Institute recommends a full physical inspection and updated reserve study at least every three to five years, with annual financial updates in between to adjust for actual expenditures, changes in interest rates, and updated cost estimates. Some states have codified specific requirements — Florida's recent legislation, for example, imposes mandatory inspection and reserve funding requirements on condominium associations. Beyond regulatory minimums, communities should consider an updated study any time a major unexpected expenditure occurs, when construction costs in their market shift significantly, or when the board has reason to believe the current funded status does not accurately reflect the community's actual financial position.